Or, Some Early Investigations into the History of Delaware’s Revenues, with Particular Attention to Corporate Franchise Fees

Value of the Franchise – Research Note #1

Today, many Delawareans (and esp. state politicians) consider maintaining the state’s dominance in corporate registrations to be one government’s most urgent tasks. Having an outsized number of outside companies domiciled in the First State supplies a hefty portion of state revenues – $1.3 billion in franchise fees alone in 2025, nearly 20% of total revenues for that year.

Delaware’s dependency on outside businesses for government funding makes the state unique – and perhaps uniquely corrupt, too – but the situation also raises some urgent historical questions. Namely: how long has this been going on?

To hear Delaware’s current judicial, legislative, and executive officials tell it, Delaware’s current situation is of ancient standing, defining its political economy since at least 1911, when New Jersey supposedly “lost” the registration game, or perhaps even 1899, when Delaware changed its corporate law to attract more fee-paying registrants.

But I’m a historian; a lot of water has passed under the bridge in 127 years, particularly when it comes to how American states organize and pay for themselves. Is the common wisdom of Delaware today true? Has the Small Wonder really had its political economy stuck in amber for more than a century?

To find out, I went looking for data that could help put Delaware’s current, desperate efforts to maintain it’s corporate franchise in context. And I found some!1 And now I’ve got information on Delaware state revenues, 1880-2024, from two series (see note on sources, below, for details).

What follows is a first pass look on patterns that jump out, illustrated with some ugly graphs (because I don’t know yet how to make nice ones).

~~~

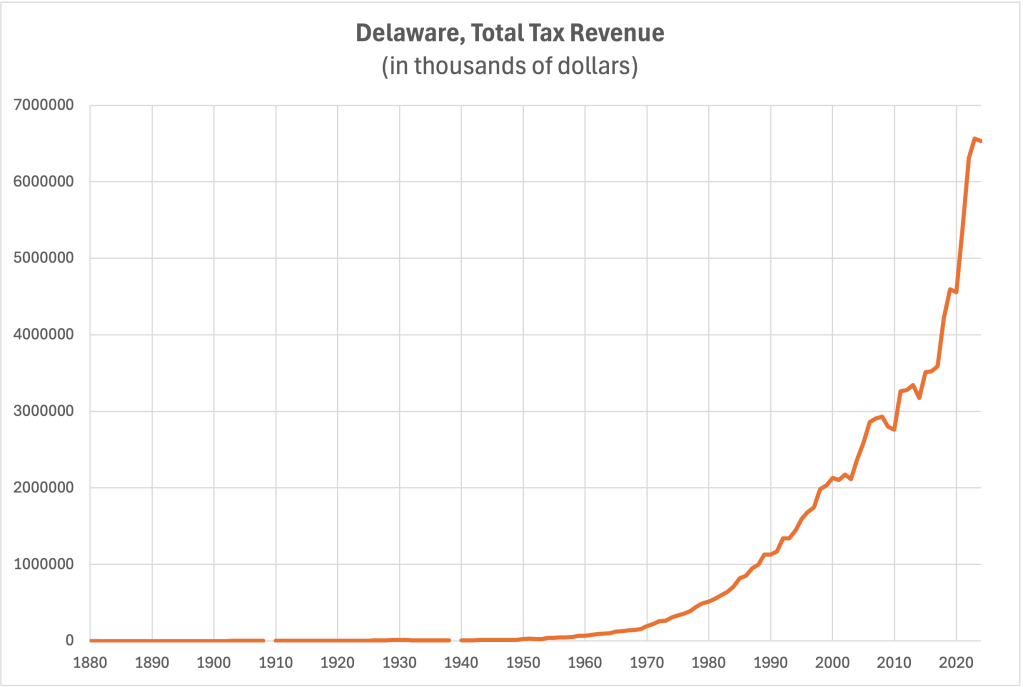

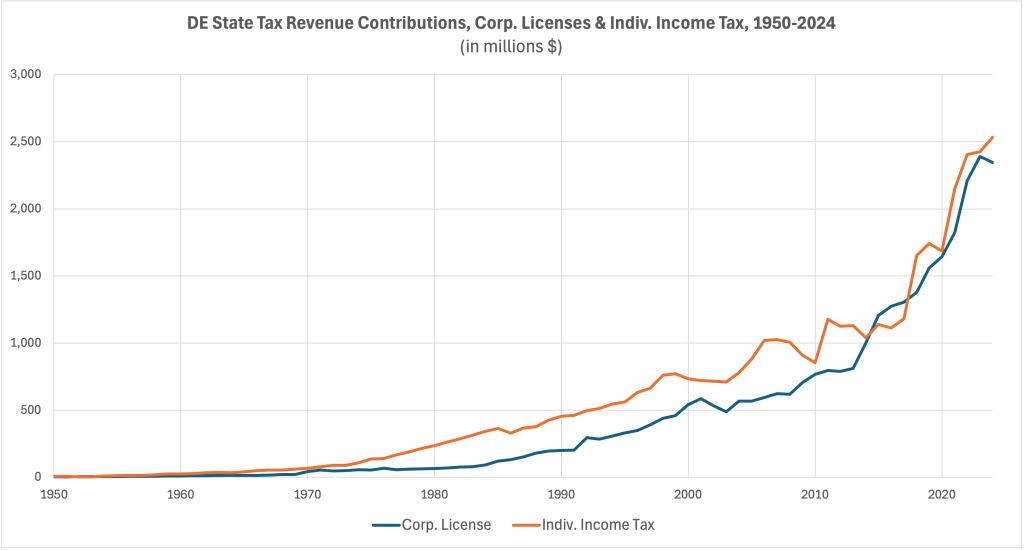

First: the fiscal resources captured by Delaware’s state government through taxation have dramatically increased since WWII, with an especially steep rise since the turn of the 21st century. This graph illustrates some of that change.

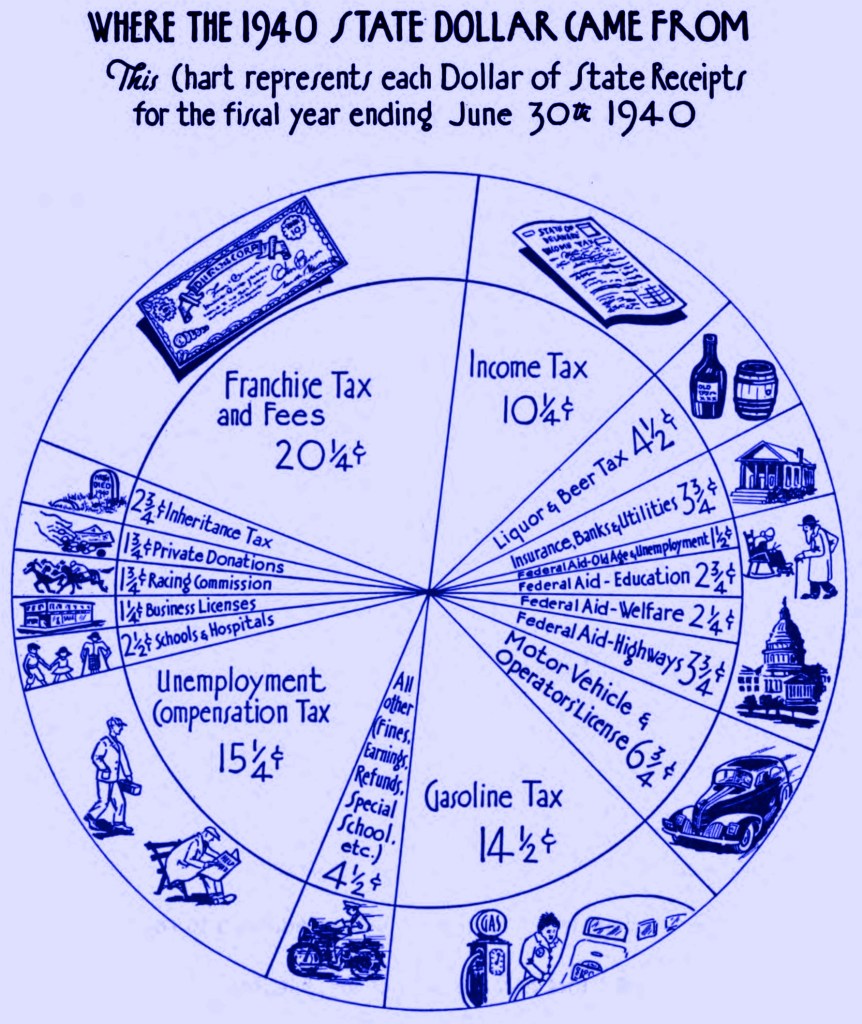

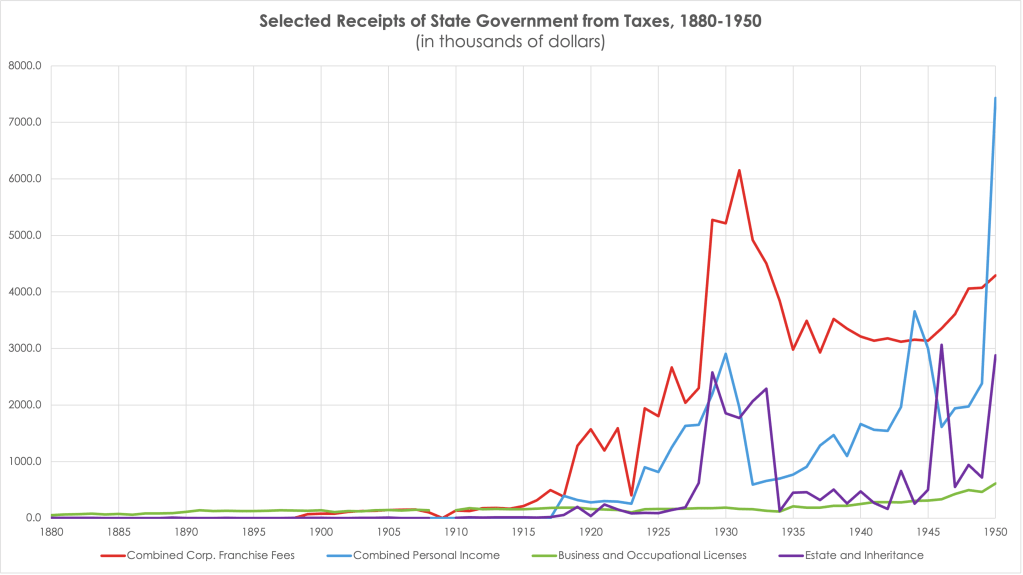

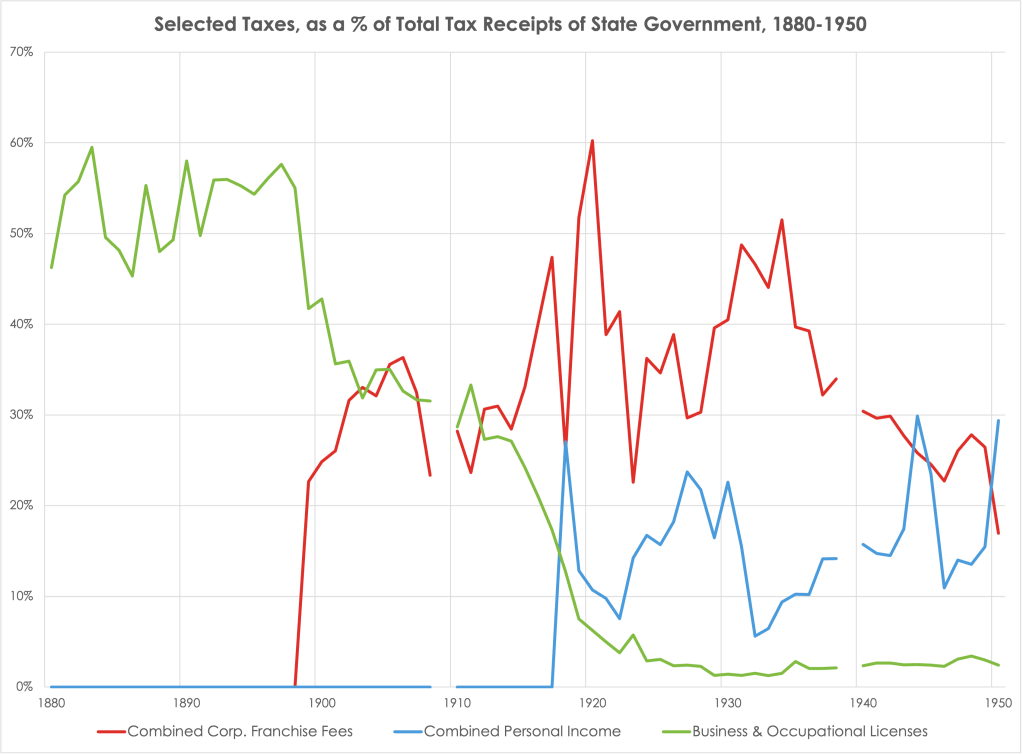

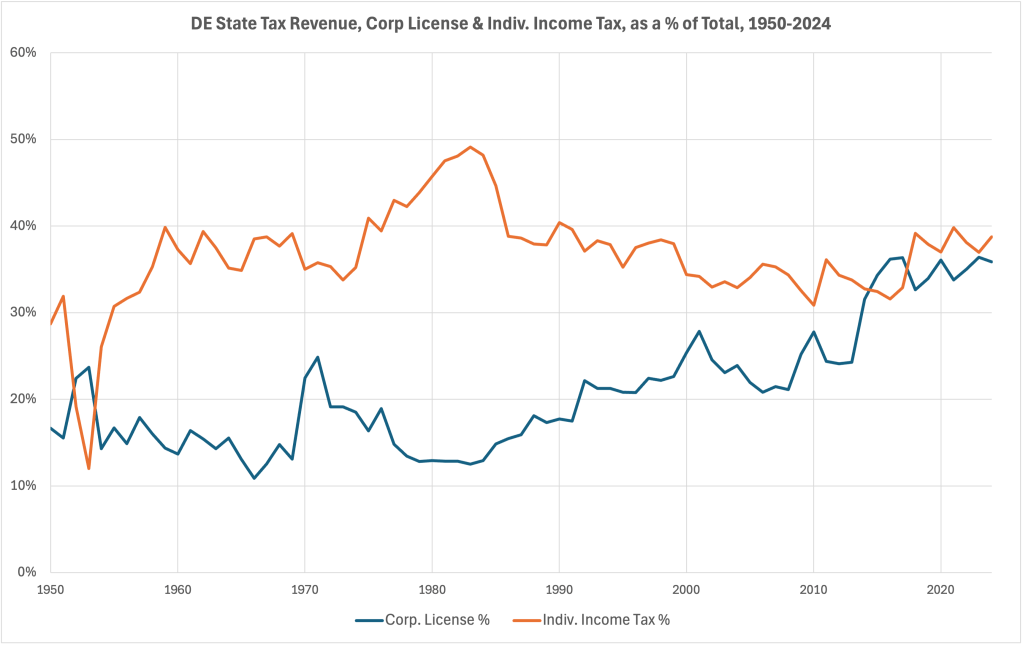

Second: Delaware’s revenue mix changed dramatically in the 1910s. Prior to WWI, the state’s overall revenues were quite small, and business and occupational license fees accounted for a clear majority of them (that is: things like barber’s licenses). The introduction of corporate franchise fees in 1899 changed that – but only after war kicked off in Europe did the franchise start kicking in more than official permissions to give haircuts. These growing franchise revenues were additive: other revenue sources did not disappear, but instead combined to grow the entire pie – which rose still higher starting in 1919 with the introduction of personal income taxes and hikes in the inheritance tax.

Third: Postwar, individual income tax revenues routinely outpaced the total dollar contributions of the corporate franchise and its percentage of total revenues. That’s the “normal” of modern Delaware: for 70 out of 75 years covered by this data (1950-2024), income taxes contribute more to state revenues than the corporate franchise – and usually 2-3X more.

That gap is large in the immediate postwar decades, but starts to narrow steadily in the 1990s – and 2015, the corporate franchise’s contributions briefly outpace individual income taxes again. The current status quo, where the franchise is as important, or nearly so, as personal income taxes dates from the post-2008 crisis era, aka the Markell administration

So how long has the State of Delaware been dependent on the corporate franchise? It depends. The franchise has contributed substantively to state revenues since its inception, and, at times, provided the a clear majority of fiscal resources. Too, the growth of the corporate franchise tracks closely with the expansion of the state government of Delaware – insofar as our little backward province has a modern fiscal apparatus, it’s origins and development are coincident with the franchise.

But! The current status quo, where corporate franchise fees account for a third of total tax receipts is a relatively new circumstance. That is: the state’s deep dependency on oligarchs’ whims is younger than Zoom, more recent than the MCU – more youthful, even, than my undergraduate students. Which suggests that it’s something that could be unwound, or at least altered – if Delaware politicians wanted to expose themselves, and residents of the state, to less extreme exploitation from the richest of the rich.

—— Header image source:“State of Delaware: Where the 1940 State Dollar Came From,” Annual Report of the Delaware State Tax Commissioner, 1939-1940 (Dover, DE), p. 26.

A Note on Sources:

I drew on two sets of sources to compile a dataset on Delaware state revenues from 1880-2024.

These printed reports are idiosyncratic: their contents depend, in large part, on the whims of the State Tax Commissioner. I drew from two specific reports that featured an especially detailed series of historical data on tax receipts, 1880-1950: 1930-940, pp. 34-35 and 1950, pp. 18-19. While later reports are extant – even digitized through to 1970 – they tend to report annual data only, and not longer historical series.

Though it draws on state officials for data, the Census Bureau organized that data slightly differently, using standard categories rather than state-specific terms. (What in the Delaware State Tax Commissioner’s hands is often denoted as “Corporate Franchise” revenues are in the STC described as “Corporate Licenses.”) Though the STC includes a few scattered datapoints for the 1940s, the records run in series only from 1950 to 2024.

Neither of these series provided data on other state revenues that derive from corporate registrations, like escheatment; that’s a significant blind spot, as some of these have paid out hundreds of millions into the state treasury in recent years.

While this dataset is extremely detailed, and includes many different details on the specific funds revenues feed into, as well as categories, divisions, and departments, it goes back only to 2017 – a few years after one of the major shifts in the importance of the franchise to state revenues, overall.

—

Well, eventually I did, in print sources and online datasets. That was after I visited the Delaware Public Archives to try and locate historical tax records – an effort proved to be a waste of time because the State of Delaware does an awful job when it comes to recording and archiving its past revenues, either in their original format or even the annual aggregate reports. (When it comes to government reports, most executive department records are organized by Governor, and held in that officials’ personal papers – and mixed together willy-nilly with all kinds of other material, like dinner invitations, like the state is some kind of medieval kingdom.) It may be these records exist in more or discoverable or usable form, but I’ll be damned if I could figure out where they are. ↩︎

Fenwick Island, as a modern community, was born a Delaware chartered corporation – which perhaps explains the municipality’s current attachment to corporate voting.

Today, the Town of Fenwick Island is (in)famous for being among the handful of Delaware municipalities that allows corporations to vote in local elections.[1] Like other towns that enfranchise fictional persons, Fenwick awards voting rights on the basis of residency and property ownership. The tiny beach settlement (year round pop. < 400) does put some limits on the corporate vote: since 2008, Fenwick’s charter has insisted on a “one-person/entity, one vote” principle, so property owners cannot double dip, voting as both individuals and as the entities they control; nor can they vote multiple times based on the number of parcels they (or the entity) own.[2]

Still, the political community that defines this narrow spit of land is firmly committed to oligarchy. Not only are non-resident property owners enfranchised, they can – and frequently do – make up a majority of the town council: only three of its seven members have to be full-time human residents.[3]

Recently, Fenwick was in the news for more than its generic lighthouse. In December 2025, the ACLU Delaware sued Fenwick in state court for violating the Delaware Constitution’s guarantee of “free and equal” elections conducted on the principle of “one person, one vote.” [4] The case is pending, though Fenwick Mayor Natalie Magdeburger told a reporter that it is “[o]ur belief is that everyone who pays taxes and is subject to our ordinances should have a vote” – including within “everyone,” the artificial entities commonly used to manage property. [5]

But how did this one-lane sea shore village become a rentiers’ redoubt? And when did it decide to shift from human rule to government for and by artificial entities? The legal history of this sandy spit on the Mason-Dixon line reveals the surprisingly recent roots of corporate voting, as an active practice – but also Delaware’s long tradition of privileging property over people.

~~~

Fenwick Island began its life as a distinct Delawarean community as an insider real estate speculation. In 1893, John H. Layton, Clerk of the Delaware House, bought out the owners of the barrier island that overlapped the Delaware-Maryland border, commonly known, if vaguely, as “Fenwick Island.”[6] Layton appears to have been the front man for a consortium of moneyed Delaware speculators, including legislators and industrialists, who quickly won two corporate charters to develop and manage the property.

The first, the Fenwick Island Company, was a real estate firm dedicated to managing “the business of purchasing, selling, holding, improving and managing real estate and island property.” The state granted it a $50,000 capitalization, extendable to $300,000, and the right to construct a railroad. (NB: unlike corporations under current Delaware law, the Fenwick Island Company’s founding document guaranteed shareholders’ democratic governance rights: all bylaws had to be decided by stockholders, and at all stockholder meetings, “all questions shall be decided by decided by a majority of votes case…each share of stock being entitled to one vote.” No question about rights to make proposals then, though later corporate advocates committing acts of law office history have offered alternate facts.)

The second was the Fenwick Island Gunning Club. Though Fenwick’s dunes and marshes were reportedly good territory for goose and duck shoots, its charter was silent on “gunning” (hunting) – but it did declare the corporation’s purpose as to provide for the “social intercourse and mutual improvement of its members.” (It’s founding members were the same as the real estate company.) [7]

Despite Layton’s string-pulling in Dover to acquire land and investment vehicles, not much came of the effort. Fenwick land sales didn’t boom, and neither a hunting resort nor a railroad was built. But in the decades following, Fenwick Island did become something of a cheap vacation spot, the site of regular evangelical camp-meetings, where vactioners enjoyed shore stays in rustic lean-tos and squat cottages [8]. After the state built a new road in the 1930s, cottagers petitioned for the right to purchase titles to the lots they leased – which they gained in 1942, after a legal battle over property rights between the state and the various “real estate men” resolved in the state’s favor.[9]

~~~

By 1953, the growth of Ocean City, Maryland next door, and the advent of better roads and more secure land titles, appears to have made Fenwick popular enough to lead property owners to petition the General Assembly for a charter, which duly passed into law without attracting comment. As with the corporation that preceded it, the town was to be run for and by property. Its government, a town council, was a body whose membership could only be composed of freeholders; those town councilors would be voted in by an electorate composed of “male or female” persons, twenty-one or over, who qualified for the franchise by being “freeholders,” either themselves or by marriage. Notably, while the original Fenwick Island town charter explicitly recognized that persons, partnerships, and corporations could be assessed taxes, implicitly it reserved voting rights for “persons” with qualities of gender and age – that is, human beings. [10]

Unusually for Delaware municipalities, the Town of Fenwick Island has never revised its charter wholesale, but only amended it – making it more difficult to track when corporate voting arose. The first evidence of the practice in state law appears in 1965, when the town charter was amended to allow the authorities to issue infastructure bonds. As with other municipalities, this new capacity for extending municipal credit came with new oversight: special hearings to propose and discuss the borrowing, and a special election to obtain voters’ approval. These special bond elections expanded the electorate to corporations, explicitly, and tilted power toward wealth: “every owner of property, whether individual, partnership or corporation” could vote, and they “shall have one vote for every dollar” paid in tax. Voting could be in person “or by proxy.” In other words: a few months before the US Congress would pass the Voting Rights Act to ensure all Americans could participate in elections equally, the Town of Fenwick Island in still-segregated Delaware extended new voting rights only to propertied fictional persons. [11]

Universal human suffrage did not reach Fenwick Island until after man had visited the moon and disco conquered the dance floor. In 1979, a charter amendment lowered the voting age to eighteen, and specified that all humans residents in town on election day were “entitled to vote.”[12]

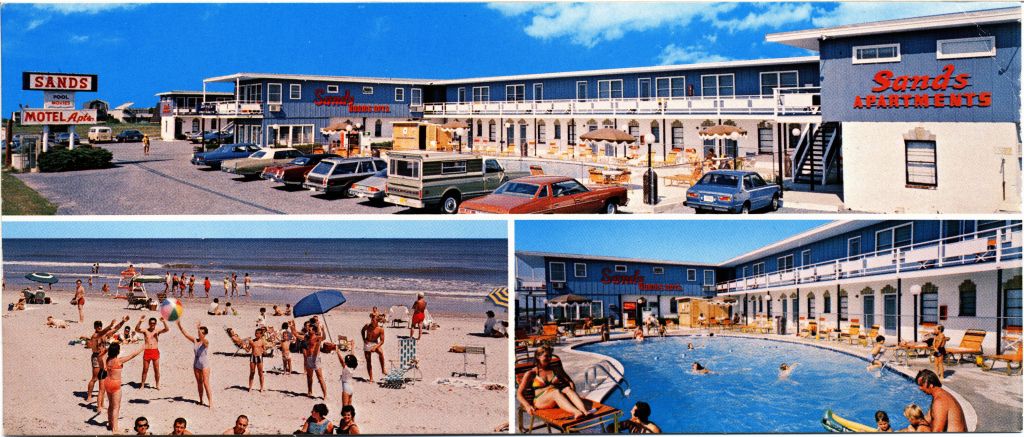

This new regime was not without its complications, however. In 1981, Fenwick’s police chief, James L. Cartwright, was disqualified as a candidate for a town council race because he did not own a sufficiently decisive property interest. A non-resident, Cartwright had thought himself qualified, because he owned a minority stake in a corporation that owned real estate in town: 20/400 shares in the Sussex Sands Inc., a corporation that owned and operated the Sands Motel. Citing an unpublished “municipal policy” that granted only majority stockholders of property-owning corporations the right to run for office, the town council rejected Cartwright’s bid for candidacy – and he found a lawyer to contest the rejection. His attorney, Robert C. Wolhar, discovered that “at least three of the current councilmen” in Fenwick were similarly deficient – owning only a minority share of the same motel corporation. A town council thusly improperly constituted, Wolhar alleged, could not govern legally, and thus “all the ordinances and police arrests made in the small seaside town may be illegal because some of the commissioners … were seated illegally.” [13]

The Delaware Department of Justice, following its characteristic approach to white collar law enforcement, declined to pursue the matter. The next Fenwick election – with a high turnout of 400 – swept in a slate of fully qualified candidates, seemingly resolving the immediate issue.[14] Following this dispute, Fenwick amended it’s charter several times in the early 1980s, using increasingly convoluted language to define qualifications for voters and candidates for office. In 1986, it settled on the exclusion of “freeholders” who “who claim title to real property by virtue of their ownership rights in a limited partnership, a corporation, or other fictitious name association, or in special circumstances, where an organization is formed for the apparent or express purpose of taking title to property principally to acquire the right to vote, or a person or persons who claim title to less than 50 percent of the real property which is owned jointly with a corporation, limited partnership, or fictitious name organization.”[15] How the town council was to discern the “apparent or express” purpose of a corporation was not specified.

Sidebar: Sussex Sands, Inc., the corporation that owned the Sands Motel and in which Cartwright and several town councilmen owned minority shares, remains a going concern. John Caldwell, the owner and operator of the motel (and failed town council candidate himself) died in 1982, but his widow remains listed as the registered agent for the corporation, at the motel's original address (a comparison of a 2012 Google Street View image and a 1979 postcard featuring the motel reveal the property to be the same). In 2020 the motel was remodeled and renamed, and is now branded as an upscale Hilton property, “Fenwick Shores.”[16]

The latest major change with regard to corporate voting in Fenwick Island was made by amendment in 2008. In a sweeping revision of the charter’s voter qualification section, the amendment inserted a by-then increasingly common (in Delaware) “one-person/entity, one vote,” provision, limiting both natural persons and artificial entities to one vote, total, no matter how many parcels of property they owned. It also specified more clearly the documentation needed for corporations (a notarized power of attorney designating a proxy voter; corporations still need humans to take action).

In keeping with twenty-first century Delawarean practice, the provision of corporate voting went unremarked in public discussions of the amendment process. The town manager, Anthony Carson, justified the revision only in terms of needing to increase the town’s “outdated” credit limit, raise funds sufficient to build a new “public safety building.” At least in news reports, the “one person/entity” rule – or corporate voting, more generally – did not warrant a mention. [17] A 2018 charter amendment increased the burden on human voters – requiring more identification to establish residency – but left procedures for corporate voters unchanged. [18]

~~~

Human democracy – government for the people, by the people – has never taken firm root in the sandy soils of Fenwick Island. A land imagined speculatively from its first legal organization, property has always called the shots there. Controversy over governing power, when it has occurred, has been over how much control a given person (natural or legally fictitious) has over real estate title – not whether people matter more than property.

Fenwick Island, then, mirrors in some ways Delaware’s increasingly unambiguous preference for corporate controllers over community stakeholders. Whether it’s taxes at the beach, or plaintiffs at the bar, the state’s governing institutions seem to incline to consolidated power over any other available option. It remains to be seen how this system will weather the strong storms we know are coming.

[1] Corporations and other artificial entities, including “partnerships, trusts, and limited liability companies” – provided they are domiciled in the state, and own property in the town. Charter of Fenwick Island, Sec. 9(A)(2), State of Delaware, accessed January 20, 2026, https://charters.delaware.gov/fenwickisland.shtml

[6] The newspaper reporting on Layton’s purchase is somewhat contradictory, but it appears he gained title to the island by buying out two members of the Gum family, Dr. F. M. Gum and William A. Gum, for a total of $6,750, in separate transactions. Layton’s purchase was covered in an amused tone by otherwise bored legislative reporters, who noted his enthusiasm for the property and its possibilities for duck hunting and sheep herding . “Bought Fenwick Island,” Morning News, April 10, 1893, p. 4; “Legislative notes,”Every Evening, April 18, 1893, p.1; “They Own the Whole Island,”Evening Journal, April 28, 1893, p.5; “Clerk Layton’s Purchase,”Every Evening, April 28, 1893, p.1.

There were earlier Delaware corporations with “Fenwick Island” in their names, but these appear to have been aimed at improving water infrastructure – ditch digging. See 14 Del. Laws, c. 149 (1871), “An Act to Incorporate the Fenwick’s Island Improvement Company,” March 15, 1871, pp. 217-220; 18 Del. Laws, c. 375 (1887), “An Act to Incorporate the Fenwick’s Island Beach Company,” April 14, 1887.

19 Del. Laws, c. 982 (1893), “An Act to incorporate the Fenwick Island Gunning Club,” April 24, 1893; 19 Del. Laws, c. 722 (1893), “An Act to incorporate the Fenwick Island Company,” April 25, 1893 pp. 972- 975. (On shareholder rights, see 19 Del. Laws, c. 722 (1893), p. 973-74.)

[10] “Other New Bills,”The Morning News, March 27, 1953, p.10; “Other Bills Passed,”Morning News, July 2, 1953, 40; 49 Del. Laws, c. 302 (1953), “An Act to Incorporate the Town of Fenwick Island, Delaware,” July 8, 1953, pp. 602-23 (on voter qualifications, see p.606, on taxes, p. 612).

In 1962, a Washington DC paper reporting on Fenwick’s amenities for vacationers – including a beach that coughed up silver dollars – noted that “the council is elected by everyone registered on the property tax rolls.” See: Janet Koltun, “Money Banks Deposits Dwindle but Fun Rises,”Evening Star (Washington, DC), Aug. 5, 1962, C-6

[11] 55 Del. Laws, c. 89 (1965), “An Act to Amend Chapter 302 … ‘ An Act to Incorporate the Town of Fenwick Island, Delaware’ By Authorizing the Borrowing of Money and Issuing Bonds Therefore…,” (May 27, 1965), pp. 360-62.

Greetings, I hope this finds you well. I wanted to bring a recent piece of news to your attention, as it bears on the General Assembly’s treatment of corporate law.

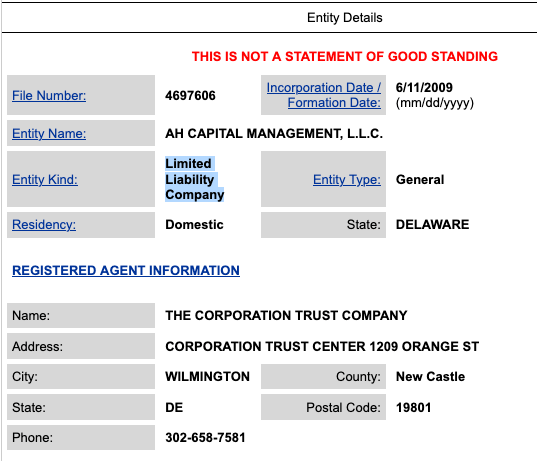

Here’s the thing, though: Andreessen Horowitz (AH Capital Management) is not a Delaware corporation. It’s a Delaware LLC.

As a limited liability company, it can’t “move” its incorporation anywhere; it doesn’t exist. More to the point, none of Andreessen Horowitz’s complaints about Delaware apply to their firm, or to any of the subsidiaries they have registered here as LLCs or Limited Partnerships (LPs), as a quick search of the DE Division of Corporation Business Entity Filing database will attest. This distinction is not a mere matter of synonyms, but one with material consequences for how a business operates. As legal scholars have observed, “An LLC By Any Other Name Is Still Not A Corporation.”

It seems unlikely that the leaders of the world’s wealthiest venture capital firm cannot distinguish between two basic types of business entity structure. It seems equally unlikely, then, that Andreessen Horowitz’s decision to leave Delaware is motivated by their stated reasons. Their critique, in other words, appears to be made in bad faith.

As you and your colleagues contemplate further revisions to Delaware’s corporate law, I urge you to keep this evidence of deceptive arguments from Delaware’s critics in mind – whether they come from business owners, directly, or the locally influentiallegal advocates they employ.

Sincerely, your constituent, DN

NB: most of the outlets reporting on this move – NYT, Bloomberg, Inc – reproduce Andreessen Horowitz’s statement without comment, and thus its errors.

Or, How U.S. Steel Now Resembles the Royal African Company – and What That Means for American Democracy & American Capitalism

How does an autocrat affect the business world? As Leviathan thrashes his bulk and churns the seas, how many adventurers’ ships do his waves swamp and founder? And how might the folks interested in those ships attempt to appease Leviathan?

The US is six months into the MAGA Restoration, and having effed around, I think we’re starting to find out.

Left: Coat of Arms of the Royal African Company; Right: Logo of U.S. Steel

~~*~~

On June 18, 2025, Nippon Steel acquired U.S. Steel for $14.1 billion dollars, making the long-lived American industrial corporation into a wholly-owned subsidiary of the Japanese company. The deal to create the world’s second-largest steel operation was a long-simmering one, running over eighteen months, largely due to federal opposition on “national security” grounds, first from the Biden administration and then the Trump regime.

The impasse broke in mid-June, when the companies involved found a novel way to satisfy Trump’s vanity: they promised him a powerful, personal “golden share.” Journalists at the NYT, Bloomberg, WSJ and elsewhere all reported – seemingly only on the basis of company-issued materials – that holding this “Class G share” would grant President Midas-Touch unusual power over the operations of the new subsidiary, still to be named U.S. Steel.

“Nippon Steel and U.S.Steel struck a National Security Agreement with the US, in which US Steel will issue a so-called golden share to the government. The golden share gives consent rights to the US president concerning reductions in capital investments, changing US Steel’s name and headquarters, redomiciling outside the US, transferring jobs or production outside the US, acquisitions and decisions to close or idle existing facilities.”

Some context: a “golden share” is a special class of stock that allows its holder, typically a government, to outvote all other shareholders in some circumstances, like during proposed charter amendments. The term appears to date to Thatcher-era Great Britain, though the practice of a government assuring itself control of an important corporation by taking an ownership stake is far older (central banks, for example, often operate this way). In the contemporary moment, “golden shares” seem to function like a glitzed-up, nationalized version of the dual class shares that oligarchs, like Mark Zuckerberg and Warren Buffett, use to maintain personal control of their companies without tying up their capital in equity.

But while “golden share” structures are common outside the US – Brazil holds a “golden share” in aircraft manufacturer Embraer, the PRC owns shares of companies like ByteDance, etc – the arrangement is quite rare, and perhaps unique, in the US. Even when the federal government re-capitalizes failing companies, as it does during bailouts (e.g. GM’s after 2008, or any number of railroads, airlines, and financial institutions), US officials have stayed far away from using the resulting equity to assert control over operations, much less business strategy.

Instead, Article VI U.S. Steel’s new charter grants “Donald J. Trump” vast control over the operations of the company. While he is serving as president, “written consent of Donald J. Trump or President Trump’s Designee” is required for the corporation to: alter its charter, change the company name, move its headquarters out of Pittsburgh, re-domicile outside the US, change its capital investments, sell any production location, acquire any other company, implement price changes, accept financial assistance from the Japanese government, reduce employee salaries, or “make material changes to the Corporation’s existing raw materials and steel sourcing strategy in the United States.”[2]

When or if Donald J. Trump is no longer president – a future the new charter does not contemplate except by implication – these powers fall to the US Department of Treasury and the US Department of Commerce, though who within those departments can act, or how they are to act together, is unspecified.

So: Nippon Steel has provided a specific person, President of the United States Donald J. Trump, with governing power over their subsidiary corporation, a company worth (as of last week) $14 billion dollars. He holds this power not as an owner of equity, or as a director with fiduciary duties to equity owners, but simply by virtue of his office and political power.

To be blunt: is the kind of thing corporations do to satisfy autocrats. Only in a personalist dictatorship do you give the head of state a role in your foundational corporate charter; it’s a courtier’s pact, made to curry special favor, and bind a political patron to the business.

No, what’s odd about this U.S. Steel deal is that the Trump regime appears to have arranged personalized governing power over a corporation, without acquiring ownership. They seized the opportunity to assert sovereign authority over a national enterprise, through a single person, not an owner’s property rights. In U.S. Steel, they have recreated the powers of a king.

~~*~~

There are many ways to think about the shape that business takes in an autocracy. We don’t lack for models: from the Congo Free State under Leopold II to Jim Crow Mississippi to fascist Italy or today’s PRC, there are diverse examples of how capitalist expansion continues – and, arguably, thrives – under despotic rule of many different types and in many different places.

But this U.S. Steel disaster resonates with a deeper history, I think, the place and period of where capitalism first emerged, alongside – and in partnership – with ambitious autocrats: early modern England. At least, there seem to be several familiar chords in this music. First, in this period, the British (neé English) empire relied on corporations as a critical tool for colonial and commercial expansion – corporations that, for the most part, were created by the Crown, not Parliament. Second, the early British empire was quite unstable, riven by repeated cycles of revolution and restoration, coups and counter-coups – which provided lots of opportunities for negotiating and re-negotiating the relationship between state and corporations, monarchs and market institutions, and a lot of explicit writing and wrangling about what these relationships could, should, or did mean.

Finally, the autocrats of the period – and in particular, the well-coiffed but fragile-necked Stuart kings – provided the whetstone against which early Americans, and their political heirs, sharpened their ideas about liberty to a cutting edge. It’s a period rich in relevant material, as well as direct influence, on the politics of our present moment.

Which brings me to the Royal African Company. The RAC was a joint stock trading corporation with a monopoly on all English trade with West Africa. First granted letters patent (e.g. a charter) by Charles II in 1660 under the title “Company of Royal Adventurers into Africa,” it took on its more well-known name, and some additional powers, with a re-chartering in 1672. [3]

The RAC was, in many respects, a bog standard corporation of its time and place. It was one of dozens of companies chartered in 17th-century England, and like the Levant Company, the East India Company, or the Hudson’s Bay Company, its charter not only granted its associates unified legal personhood – and thus the ability to concentrate and deploy capital beyond the means of any one merchant – but also monopoly rights over a specific trading territory, and governing power there. Like these other companies, the RAC was explicitly a tool for colonization and imperial competition: it could establish forts, manors, and plantations, set up courts, and develop, marshal, and maintain military force on land and sea, as needed to fulfill that purpose.

While it’s fashionable in corporate law and finance circles today to approach corporations as organizations with ultimately “private” origins that the state must, reluctantly, regulate to maintain the basic health, safety, and financial transparency standards markets need to function, the RAC reminds us that this libertarian conception of corporate life is detached both from historical reality as well as the letter of the law. Like modern corporations domiciled in Delaware, the Royal African Company was a subdivision of the state, a temporary division of sovereign authority, granted to a body of subjects to accomplish a purpose – and therefore ultimately and always a creature of government, in all senses. [4]

Two things made the RAC unique, amid this host of incorporated adventuring companies. First, while the company’s initial business was the gold trade, it quickly – and quite successfully – expanded into slave trading. Indeed, a few years into its existence, the RAC became the dominant player in the trans-Atlantic traffic in human beings, and over its life it shipped more people across the Atlantic into chattel bondage than any other single institution. [5]

Second, from its first charter onward, the company’s lead founder and “first governor” (e.g. board chairman and CEO) was the king’s brother, James, Duke of York. And James… James was a special guy. Amid some serious competition from his grandfather, father, and elder brother, James Stuart, Duke of York and (briefly) King James II (of England and Ireland) and VII (of Scotland) distinguished himself for his zeal for building an absolute monarchy based on the divine right of kings – and, unsurprisingly, also by his penchant for cruelty and the brutal persecution of his critics.

While James II didn’t meet the sharp end his father did – he fled England before anyone could effect the traditional familial separation between head and body – his time as Duke and then King made a lasting impression on British political development, as an example of what not to do. Following his fall, the power of British kings was forever broken, more tightly circumscribed by law and kept in check by the active exercise of sovereign power by Parliament.

Why? Well, all the Stuarts had been committed a project of centralizing power under the Crown, and growing the monarchy’s bureaucracy at the expense of other governing institutions. Briefly checked by the loss of Charles I’s head and the interregnum, the post-Restoration Stuarts doubled down on the monarch’s right to arbitrary authority. So under Charles II, the monarchy took to simply disappearing troublesome subjects to foreign prisons “beyond the seas” – a practice Parliament attempted to circumscribe by legislating habeas corpus in 1679. And because James II was the last – and arguably the most aggressive – champion of this project, he receives particular opprobrium for it. As historian Holly Brewer has recently reminded us, James II expanded on his family’s efforts, efficiently corrupting the judiciary with patronage in order to remove any check on the monarch’s whims. (A tune that should sound familiar to modern Americans…)

But back to the RAC: James’s executive role in the company was not in name only. He used the company to advance his colonial projects all over the Atlantic world, as a means to supply the slaves that his colonial adventures in North America and the Caribbean needed to profit. And he also wielded state power on its behalf – directing the Royal Navy to seize African forts during wars against the Dutch, for example. (Among other wartime accidents, these Anglo-Dutch conflicts led to James, as the Duke of York, briefly becoming the proprietor of the tiny, failing sub-colony of Delaware – a disappointment to all involved, surely).

In practice and in theory, there was no clear line between the operations of the RAC as a capitalist enterprise, and James’s personal exercise of autocratic power. Indeed, they co-constituted each other – with humanity all the worse for it.

But what does the Royal African Company have to do with U.S. Steel? I would argue there is a similarity in political shape. The grant of governing power to a ruler is not an act undertaken in a political economy defined by free enterprise and universal rights; it’s not even the kind of play one makes in a robust oligarchy. Rather, it’s the move a board of directors makes when playing court politics, in a monarchy.

Too, the fact the Trump and his minions worked to produce this outcome – and not a simple bribe – makes it worse than bare graft. It’s an enactment of the MAGA Restoration’s theory of politics, of a piece with the anti-democratic philosophy the movement’s intellectuals advocate, the same philosophy that’s leading the regime to crush universities, the press, and tighten its chokehold on the federal courts and Congress. It’s a politics of absolute monarchy akin to what the Stuarts and their lackeys celebrated as divinely justified (an apologia constantly offered by Trump supporters, too). That autocracy has now come to corporate America.

But despite it’s best attempts, tyranny is never the only game in town. The House of Stuart was nearly a century fled from Britain’s empire, and their pretense to rule equally dead, when the American Revolution took its first percussive bloody breaths on Lexington Green. And yet, the Stuarts’ shade remained, substantial enough to cast a defining shadow when American patriots submitted a “history of repeated injuries and usurpations” to a “candid world” to demonstrate the “absolute Tyranny” of King George III. As they sought to justify themselves for rising to rebellion and declaring independence by reference to the King’s outrageous acts (like “transporting usbeyond Seasto be triedfor pretended offences”) American revolutionaries recalled and remade a political language first articulated by by a group of seventeenth century anti-Stuart partisans, the “Country Whigs,” within a broader European discourse about the necessarily popular roots of political order and legitimacy (e.g. “republicanism”). Stuart tyranny was the lens through which revolting colonials observed the actions of King George and Parliament, and it served as the foil to the English liberty they sought to restore through rebellion.

Americans identified the dangers of arbitrary monarchical rule in part through its corporate manifestations. The Tea Act, the legislation granting the East India Company a monopoly on tea sales in North America and laying a small tax on tea to pay for government bureaucracy, was condemned by Massachusetts Whigs as a “master-piece of policy for accomplishing the purpose of enslaving us.”[6]

That sounds like a wild overreaction to tax policy – and a weird reason to destroy millions in fragrant property – until you understand that like other British colonials, Massachusetts activists saw political events through the lens of Stuart abuses. A corporate monopoly, designed to generate taxes to fund state action, wasn’t just a discrete policy, but a conspiracy to undermine the imperial constitution and drown free men’s liberties. How did they know? Their political forefathers had lived through it one before, and written a great deal about it – and those essays survived and circulated widely among the politically engaged colonial elite; and too, the colonies they inhabited took the shape and form they did in no small part due to the actions – and reactions – to James II’s wielding of corporate power.

Based on their understanding of the Stuart example, they thought the leviathan’s bulk was necessarily nourished by blood flowing through corporate veins.

Thus, the legacy of the Royal African Company, and the importance of its corrupt echo in the corporate structure of U.S. Steel lies not only in the personal despotism these companies actively embodied or embody. It rests also in the liberatory ideology that tyranny inspired, as an instrument that detects corruption in the body politic as the rot sets in, identifies it as a danger to free people, and provides the means – the words and the actions – through which it can be opposed, and destroyed.

The best way to survive a cancer is to catch it early, and treat it. U.S. Steel’s new charter shows up as a large malignant mass on America’s scan; will we be willing to cut the tumor out before its too late?

[3] For the 1660, 1662, and 1672 charters of these corporate entities that became the Royal African Company, see Cecil T. Carr, Select Charters of Trading Companies, A.D. 1530-1707, Publications of the Selden Society (London: B. Quaritch, 1913), pp. 172, 177, and 186 et seq.

[4] The source of “sovereign” authority was disputed, however. In theory, in the US today “the People” constitute “the state,” which creates corporations (state and federal). In seventeenth century England, however, the Crown asserted that authority, through the sovereign body of the monarch – though, at various moments Parliament also claimed that authority too, leading to some rather nasty civil conflicts, coups, counter-coups, and counter-counter coups, that were only resolved once the Dutch got involved – a messy outcome.

[5] The RAC shipped some 150,000 people during its primary years of activity, from 1672 to the 1720s. William A. Pettigrew, Freedom’s Debt: The Royal African Company and the Politics of the Atlantic Slave Trade, 1672-1752 (Chapel Hill, NC: The University of North Carolina Press, 2013), p.11.

However, British slave trading would soar to all-time world-historical highs only after the RAC’s monopoly was broken. Independent British slave traders then far surpasses – in a shorter amount of time – the human trafficking of every other slave-trading Atlantic nation. The end of the RAC’s monopoly was a development that planters in North America welcomed, by the way, as now they had cheaper sources for slaves. Another example of the magic of the free market, a blood-soaked sort of necromancy.

The rationale for this rash action is fear: fear that if Delaware does not extinguish judicial independence to better fit Musk’s perverse desires, Delaware will lose critical revenues, as Musk leads corporations to “DExit,” or registering in other states, because of Chancery Court decisions that since 2022 have supposedly upset the balance of power between shareholders and corporate managers.

The data does not support the panicked narrative that SB 21’s supporters have been promoting, however. That narrative seems to be a product of Musk, and his paid agents, spreading misinformation like a miasma across the state.

Delaware’s Corporate Franchise is a Volume Business

Delaware benefits in several ways from having outside corporations registered here. The most valuable benefit is revenues from the “corporate franchise tax.” This is a fee that corporations headquartered outside the state provide Delaware for the “privilege of being incorporated in Delaware.” (Fiscal Notebook, 2024 ed, p. 108). In recent years, the corporate franchise tax, alone, has provided ~20% of total state revenues, or about 1.2 billion dollars. (Personal income tax, paid by human people, provides 33% of the total state revenue). (Fiscal Notebook, 2024 Ed, p. 32).

The critical thing to know about the corporate franchise tax is that it is not an income tax: it’s a set of tiered fees, assessed based on a corporation’s total number of authorized shares – but with a max payment cap of $250,000.

In other words, Delaware is in a volume business, not a value business. Delaware has – or rather, should have – an interest in appealing to the largest number of corporate registrants, not the wealthiest billionaires. That’s a critical point, because the interests of most corporations – and most investors – do not align much at all with the desires of oligarchs like Elon Musk. If it wants revenue, Delaware shouldn’t be catering to the tiny cohort of vampires.

Back to Delaware politicians’ panic: you would think if the corporate franchise tax revenue is indeed in peril – if the “DExit” movement is real, and not just a propaganda hallucination – then there would be some data to support that claim.

Alas for Musk et al., and their well-paid agents, three data points suggest the opposite is true.

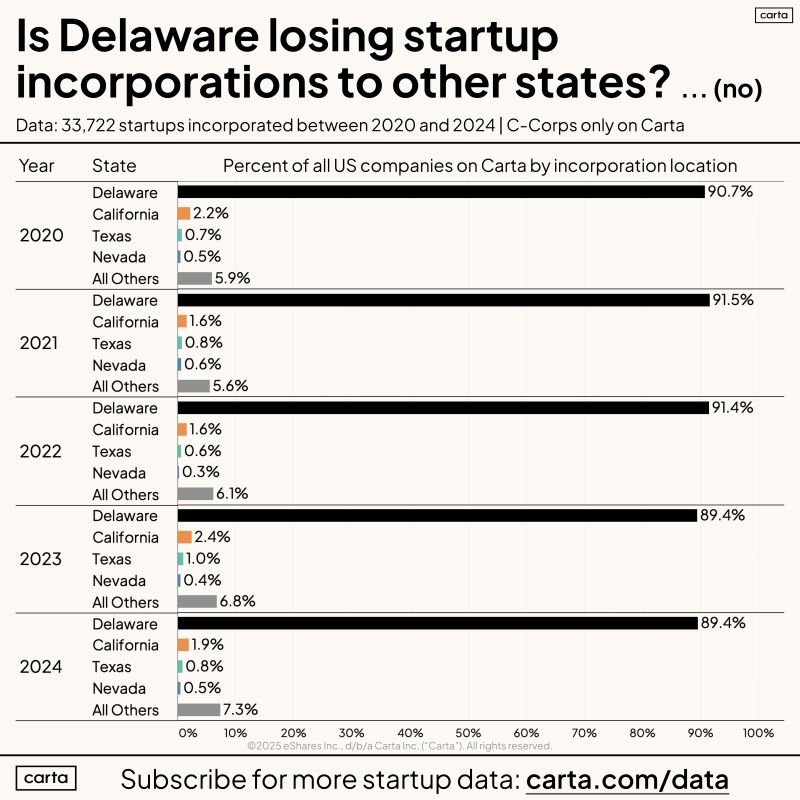

1) Startups Continue to Choose Delaware

Peter Walker, “head of insight” at Silicon Valley data infrastructure firm Carta, recently shared a chart from his company’s private dataset demonstrating that 90% of startup C-Corps are domiciled in Delaware – a percentage that has “barely shifted in the last 5 years.” Including in 2024.

2) The Number of Corporations Filing Franchise Taxes Keeps Going Up

The most recent public figures show that 309,911 firms filed franchise tax payments in FY 2024 – an increase that continues the unbroken upward trend of the last decade, before the recent Chancery Court decisions, and then through and beyond them.

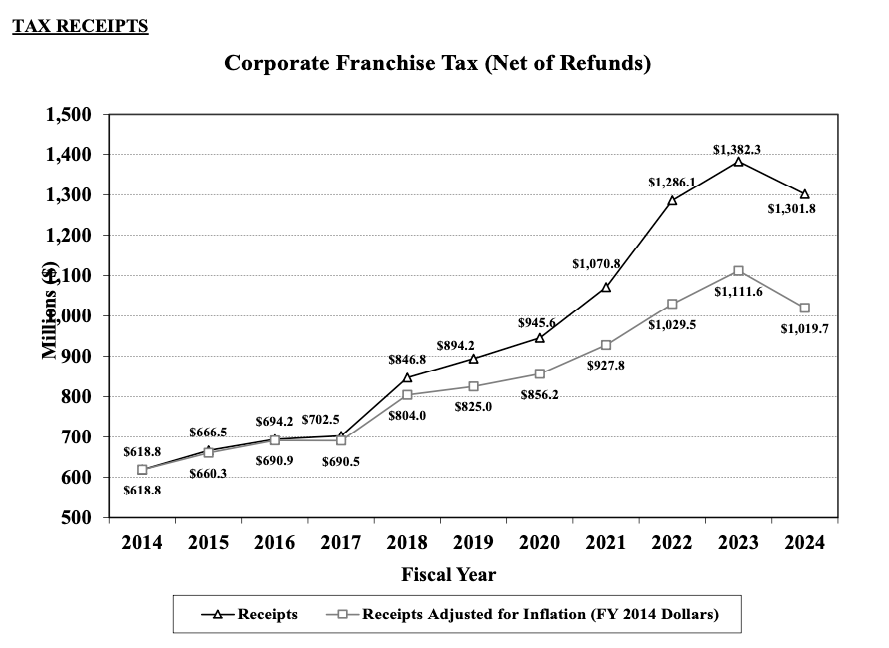

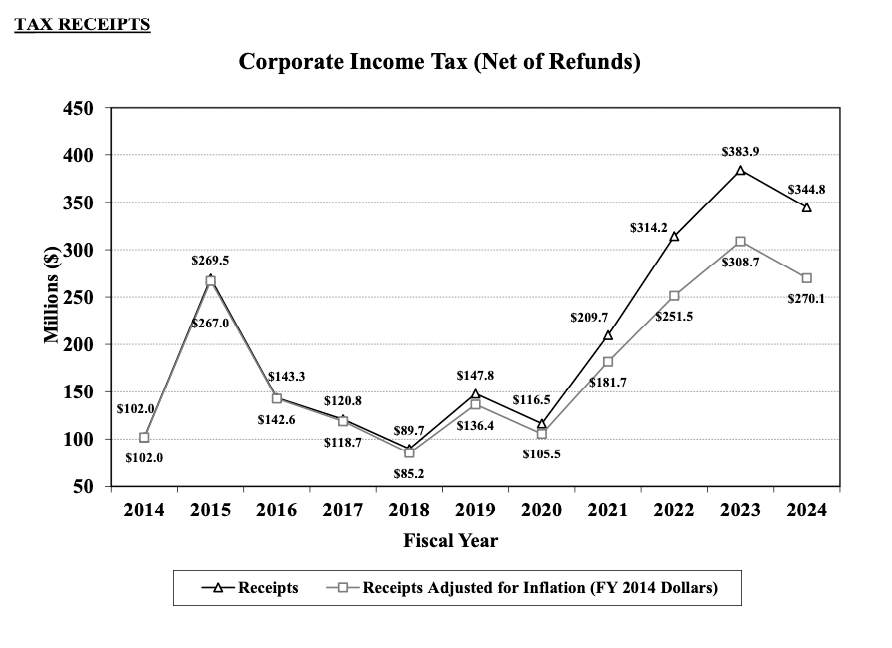

Now, total corporate franchise tax receipts have dipped, somewhat, from 2023 to 2024. But they have done so following the same patterns as the Corporate Income Tax.

Source: “Tax Receipts: Corporate Franchise Tax,” and “Tax Receipts: Corporate Income Tax,” in Fiscal Notebook FY 2024 ed., pp. 109, 115

That suggests to me that the cause lies in macroeconomic conditions – unemployment, inflation – rather than anything to do with Delaware’s legal regime. (Corporations paying income tax here do business here; they can’t exit as easily as paper registrants, and have less incentive to do so).

Since 1977, Delaware’s state government has relied on the Delaware Economic & Financial Advisory Council, or DEFAC, for economic forecasts. DEFAC meets quarterly to assess data, and issue guidance – guidance that the General Assembly usually regards as binding on legislation.

At the December meeting, DEFAC forecasts steady franchise revenues for FY 2025, 2026, and 2027. That is consistent with economic indicators – at least, prior to Musk’s installation as co-president – and suggests this expert body saw no threat in the data of the sort SB 21’s draftees were already hallucinating.

Musk’s Pungent Miasma is Not Reality

In short, private and public data sources agree: there is no observable decline in incorporations in Delaware, and no evidence that “DExit” is occurring in response to Chancery Court rulings. Further, the advisors specifically tasked with forecasting future franchise tax revenues – that is, a body of people mostly not employed by Elon Musk – do not see evidence for dramatic change.

An alternate explanation does fit the data better, though. Elon Musk’s lawyers drafted SB 21 to benefit their oligarchic clients, not Delaware. Musk’s paid agents are breathing the bad vibe fumes they want to see in the world into existence. The odor of panic they’ve wafted into lawmaker’s nostrils is thus a miasma, in the classic sense: unhealhy and unpleasant air, produced as the unpleasant exhalation of rot and corruption, that causes feverish illness.

Delaware’s leaders should not radically revise our laws, and gut a valuable franchise, on the basis of huffing Musk’s swamp gas.

Note: while by statute, the heads of Delaware’s state agencies are supposed to provide public reports on things like the total number of corporations registered here, and revenues derived from them, in practice Delaware state government is … uninterested in transparency. Opacity is part of the value Delaware provides, apparently.

The upshot is that basic data, and foundational statistics, are often hard to get, and difficult to parse using normal methods even when located. Still, while our state government officials are intentionally(?) incompetent at communicating to the public, they have not shirked their duties completely; there are sources worth your time & examination.

While this report is not linked on the DE Finance Department’s page, you can find it at that URL. An annual report, it offers a wealth of up-to-date statistics on the fiscal situation of the government of Delaware, including revenues and expenditures, as well as detailed supplemental information on specific taxes, fees, pension contributions, bond obligations, and subsidiary agencies.

The fiscal notebook is a rehashing of much of what is in the ACFR, but summarized and more richly contextualized look at the state budget, with historical data and legislative histories. If you want to know when the corporate income tax changed, and under what legislation, the Fiscal Notebook is your guide. It has some charmingly 1990s graphic design, as well. Prior reports are available here.

DEFAC posts cryptic briefing books and terse meeting minutes, grouped by date, on this page. If you dig far enough, you can find their predictions; and if you want a bit of fun, take a look at how far off they were in their predictions (usually they underestimate revenues by quite a bit, and overestimate the cost of expenditures; there appears to be a spirally structural austerity built into their models, assuming any models actually exist beyond intuition).

In theory, under the law, this page should contain the division’s up-to-date annual reports, detailing numbers of business entities registered in Delaware, and other pertinent information. In practice, this website is a wasteland.

![Louis Dalrymple, “Uncle Sam’s Dismal Swamp,” Puck, November 15, 1893, https://www.loc.gov/pictures/resource/ppmsca.29155. Print shows Uncle Sam sitting on a log in a swamp labeled "Spoils System" from which snakes labeled "Quayism", "Bardsleyism", and "Tannerism", and noxious fumes rise in the form of shades labeled "Raumism - Pension Swindler, Crokerism, McLaughlinism, Tweedism, Prendergast - Political Assassin, [and] Guiteau - Political Assassin". Also shown among the tree roots is Charles A. Dana.](https://daelnorwood.com/wp-content/uploads/2025/02/dismalswampcrop.png?w=839)

.jpg){kind=link}

{kind=link}