Earlier this month, I published a piece in a local Delaware outlet, outlining what I think is coming down the pike to Dover in the next legislative session.

When they meet again in Dover this session, Delaware’s legislators face a real problem. Decades of dependence on corporate franchise revenues have accustomed the state, and its voters, to government on the cheap; and in an economy already primed for recession, that’s dangerous. Worse, state leaders’ history of servility has undermined their ability to resist oligarchs’ demands. As former Weinberg Center Director Charles Elson has observed, SB 21 demonstrated that spending a little money will let you “overturn a Delaware court decision” – and between that legislation, and the Delaware Supreme Court’s subsequent Musk-friendly judgement, the state’s claims to offer balanced law or objective expertise have been revealed to be merely marketing. So why would any robber baron consider Delaware’s government anything but a kept pet?

In that light, it seems clear that the question for the coming General Assembly session is notwhether Delaware legislators will bend to meet the will of outside oligarchs, but how far – and what else will break, as a result, when they do.

Greetings, I hope this finds you well. I wanted to bring a recent piece of news to your attention, as it bears on the General Assembly’s treatment of corporate law.

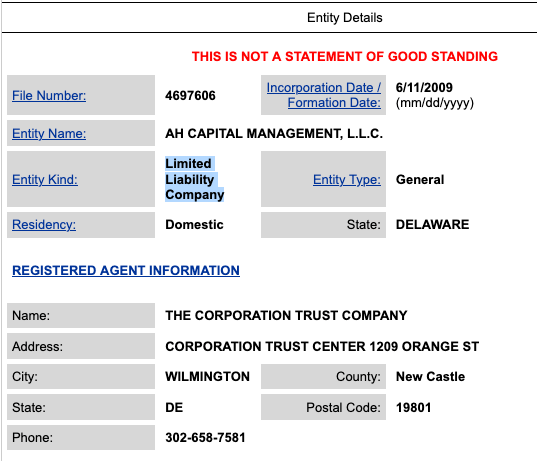

Here’s the thing, though: Andreessen Horowitz (AH Capital Management) is not a Delaware corporation. It’s a Delaware LLC.

As a limited liability company, it can’t “move” its incorporation anywhere; it doesn’t exist. More to the point, none of Andreessen Horowitz’s complaints about Delaware apply to their firm, or to any of the subsidiaries they have registered here as LLCs or Limited Partnerships (LPs), as a quick search of the DE Division of Corporation Business Entity Filing database will attest. This distinction is not a mere matter of synonyms, but one with material consequences for how a business operates. As legal scholars have observed, “An LLC By Any Other Name Is Still Not A Corporation.”

It seems unlikely that the leaders of the world’s wealthiest venture capital firm cannot distinguish between two basic types of business entity structure. It seems equally unlikely, then, that Andreessen Horowitz’s decision to leave Delaware is motivated by their stated reasons. Their critique, in other words, appears to be made in bad faith.

As you and your colleagues contemplate further revisions to Delaware’s corporate law, I urge you to keep this evidence of deceptive arguments from Delaware’s critics in mind – whether they come from business owners, directly, or the locally influentiallegal advocates they employ.

Sincerely, your constituent, DN

NB: most of the outlets reporting on this move – NYT, Bloomberg, Inc – reproduce Andreessen Horowitz’s statement without comment, and thus its errors.

The rationale for this rash action is fear: fear that if Delaware does not extinguish judicial independence to better fit Musk’s perverse desires, Delaware will lose critical revenues, as Musk leads corporations to “DExit,” or registering in other states, because of Chancery Court decisions that since 2022 have supposedly upset the balance of power between shareholders and corporate managers.

The data does not support the panicked narrative that SB 21’s supporters have been promoting, however. That narrative seems to be a product of Musk, and his paid agents, spreading misinformation like a miasma across the state.

Delaware’s Corporate Franchise is a Volume Business

Delaware benefits in several ways from having outside corporations registered here. The most valuable benefit is revenues from the “corporate franchise tax.” This is a fee that corporations headquartered outside the state provide Delaware for the “privilege of being incorporated in Delaware.” (Fiscal Notebook, 2024 ed, p. 108). In recent years, the corporate franchise tax, alone, has provided ~20% of total state revenues, or about 1.2 billion dollars. (Personal income tax, paid by human people, provides 33% of the total state revenue). (Fiscal Notebook, 2024 Ed, p. 32).

The critical thing to know about the corporate franchise tax is that it is not an income tax: it’s a set of tiered fees, assessed based on a corporation’s total number of authorized shares – but with a max payment cap of $250,000.

In other words, Delaware is in a volume business, not a value business. Delaware has – or rather, should have – an interest in appealing to the largest number of corporate registrants, not the wealthiest billionaires. That’s a critical point, because the interests of most corporations – and most investors – do not align much at all with the desires of oligarchs like Elon Musk. If it wants revenue, Delaware shouldn’t be catering to the tiny cohort of vampires.

Back to Delaware politicians’ panic: you would think if the corporate franchise tax revenue is indeed in peril – if the “DExit” movement is real, and not just a propaganda hallucination – then there would be some data to support that claim.

Alas for Musk et al., and their well-paid agents, three data points suggest the opposite is true.

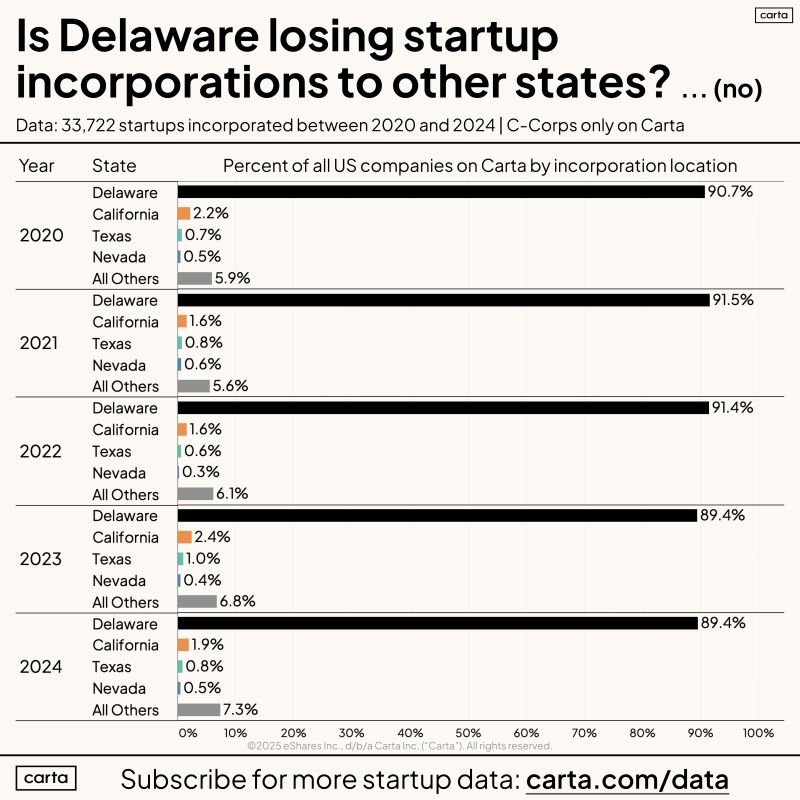

1) Startups Continue to Choose Delaware

Peter Walker, “head of insight” at Silicon Valley data infrastructure firm Carta, recently shared a chart from his company’s private dataset demonstrating that 90% of startup C-Corps are domiciled in Delaware – a percentage that has “barely shifted in the last 5 years.” Including in 2024.

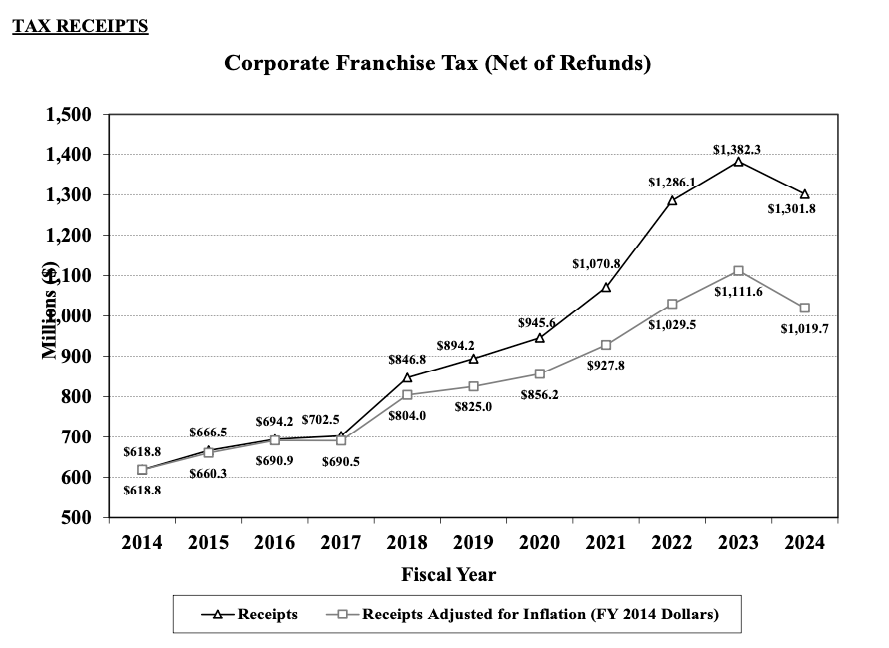

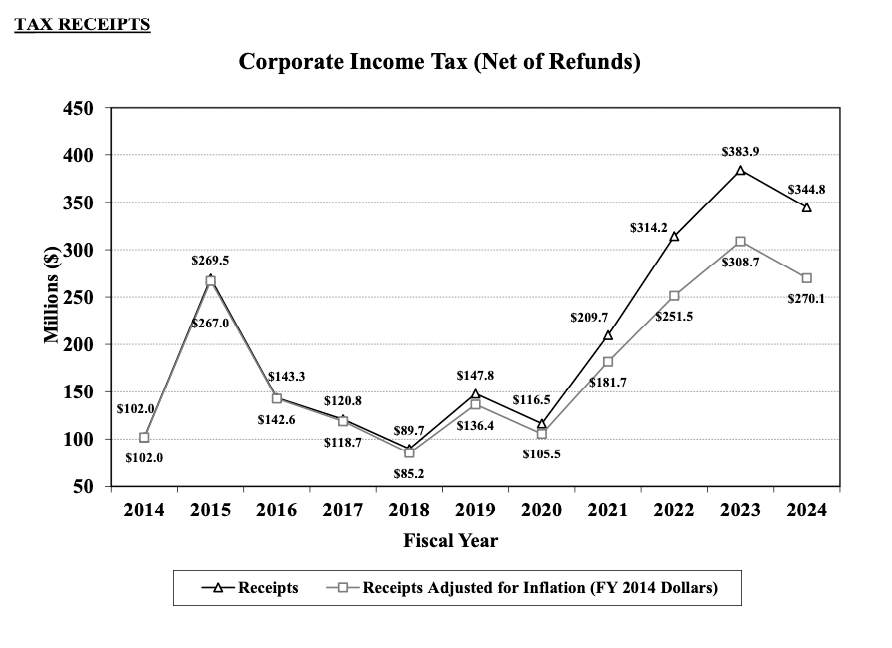

2) The Number of Corporations Filing Franchise Taxes Keeps Going Up

The most recent public figures show that 309,911 firms filed franchise tax payments in FY 2024 – an increase that continues the unbroken upward trend of the last decade, before the recent Chancery Court decisions, and then through and beyond them.

Now, total corporate franchise tax receipts have dipped, somewhat, from 2023 to 2024. But they have done so following the same patterns as the Corporate Income Tax.

Source: “Tax Receipts: Corporate Franchise Tax,” and “Tax Receipts: Corporate Income Tax,” in Fiscal Notebook FY 2024 ed., pp. 109, 115

That suggests to me that the cause lies in macroeconomic conditions – unemployment, inflation – rather than anything to do with Delaware’s legal regime. (Corporations paying income tax here do business here; they can’t exit as easily as paper registrants, and have less incentive to do so).

Since 1977, Delaware’s state government has relied on the Delaware Economic & Financial Advisory Council, or DEFAC, for economic forecasts. DEFAC meets quarterly to assess data, and issue guidance – guidance that the General Assembly usually regards as binding on legislation.

At the December meeting, DEFAC forecasts steady franchise revenues for FY 2025, 2026, and 2027. That is consistent with economic indicators – at least, prior to Musk’s installation as co-president – and suggests this expert body saw no threat in the data of the sort SB 21’s draftees were already hallucinating.

Musk’s Pungent Miasma is Not Reality

In short, private and public data sources agree: there is no observable decline in incorporations in Delaware, and no evidence that “DExit” is occurring in response to Chancery Court rulings. Further, the advisors specifically tasked with forecasting future franchise tax revenues – that is, a body of people mostly not employed by Elon Musk – do not see evidence for dramatic change.

An alternate explanation does fit the data better, though. Elon Musk’s lawyers drafted SB 21 to benefit their oligarchic clients, not Delaware. Musk’s paid agents are breathing the bad vibe fumes they want to see in the world into existence. The odor of panic they’ve wafted into lawmaker’s nostrils is thus a miasma, in the classic sense: unhealhy and unpleasant air, produced as the unpleasant exhalation of rot and corruption, that causes feverish illness.

Delaware’s leaders should not radically revise our laws, and gut a valuable franchise, on the basis of huffing Musk’s swamp gas.

Note: while by statute, the heads of Delaware’s state agencies are supposed to provide public reports on things like the total number of corporations registered here, and revenues derived from them, in practice Delaware state government is … uninterested in transparency. Opacity is part of the value Delaware provides, apparently.

The upshot is that basic data, and foundational statistics, are often hard to get, and difficult to parse using normal methods even when located. Still, while our state government officials are intentionally(?) incompetent at communicating to the public, they have not shirked their duties completely; there are sources worth your time & examination.

While this report is not linked on the DE Finance Department’s page, you can find it at that URL. An annual report, it offers a wealth of up-to-date statistics on the fiscal situation of the government of Delaware, including revenues and expenditures, as well as detailed supplemental information on specific taxes, fees, pension contributions, bond obligations, and subsidiary agencies.

The fiscal notebook is a rehashing of much of what is in the ACFR, but summarized and more richly contextualized look at the state budget, with historical data and legislative histories. If you want to know when the corporate income tax changed, and under what legislation, the Fiscal Notebook is your guide. It has some charmingly 1990s graphic design, as well. Prior reports are available here.

DEFAC posts cryptic briefing books and terse meeting minutes, grouped by date, on this page. If you dig far enough, you can find their predictions; and if you want a bit of fun, take a look at how far off they were in their predictions (usually they underestimate revenues by quite a bit, and overestimate the cost of expenditures; there appears to be a spirally structural austerity built into their models, assuming any models actually exist beyond intuition).

In theory, under the law, this page should contain the division’s up-to-date annual reports, detailing numbers of business entities registered in Delaware, and other pertinent information. In practice, this website is a wasteland.

Much like the recent revisions to state law themselves, these reactions to mild criticism are expressions of myopia. Criticism of the sort SB 313 attracted in 2024 – that it proceeded anti-democratically, that it harmed ordinary people, that it was motivated by a small set of special interests’, and would lead to abuse – were leveled at Delaware state legislators when the state’s corporate law first passed in 1899.

If anything, earlier observers of Delaware corporate law in the Gilded Age were far more blunt in their criticism than anyone in the 21st century has ever thought about being. To illustrate, lend your eyes to this brief article from the American Law Review, a legal journal based in St. Louis: “Little Delaware Makes a Bid for the Organization of Trusts,” American Law Review 33, no. 3 (May-June 1899): 418–24.

Well-known to Delaware lawyers – and recently, at least one historian – the article takes the form of an unsigned “note,” one of a few dozen that appeared at the back section of every journal issue, after the treatises and articles, but before the listings of recent major court decisions. My assumption is that it is either written by the editors, Seymour D. Thomson and Leonard A. Jones, or one of their close associates – and either way expresses their editorial views.

And my goodness, are the Am.L. Rev. editors unimpressed with Delaware trying to copy New Jersey’s loose corporate charter rules, much less their attempt to “improve” on them by giving corporations even more expansive powers. After some praise for Delaware’s old Democratic (and enslaving) political establishment (and some sharp elbows at the emerging state Republican party), the editors note that the curious feature of US federalism – that state sovereign powers are equal, and that states set corporate law – is what provides the temptation that Delaware has now given into:

“The “sovereign” States of the American Union are equal: equal in the Senate, for little Delaware wields the same voting power there as does great New York. They are also equal in regard of the deviltry they can do – equal in regard of the injury they can inflict upon their sister States. It is as though a Klondike gold mine had been discovered in New Jersey, and all Delaware were on the rush to get there. In other words little Delaware, gangrened with envy at the spectacle of the truck-patchers, sand-duners, clam-diggers and mosquito-wafters of New Jersey getting all the money in the country into her coffers, – is determined to get her little tiny, sweet, round, baby hand into the grab-bag of sweet things before it is too late.” (p. 419)

And, the editors note, this law will be a jobs-employment program for Delaware politicians; they may need to even import labor:

“But with this exception; and herein the little great “State of Delaware” casts its little great anchor to the windward. Although ” any three persons may organize a corporation,” yet ” only one director need be a resident of Delaware.” And this ” one director'” is going to be paid for being a director, and don’t you forget it. If the rush to organize corporations and trusts under this new Delaware law is as great as under the New Jersey law, there will not be politicians enough in Delaware to serve as directors of corporations and trusts for all the other States of the Union, but professional directors will have to migrate to Delaware from other States, and their name will be Legion.” (p.420)

Delaware legislators’ grandiose proclamations about their new law’s global applicability seem to be particularly grating:

” Nor will you be confined, in the conduct of your business, when so happily incorporated, to your drought-smitten and grasshopper-eaten prairies. “It,” – that is to say you when you have turned yourselves into Delaware corporations – ” may conduct business anywhere in the world.” Certainly you may. Why not? The great State of Delaware says so, and is not that enough?” (p. 421)

Halfway through, the editors re-frame their note as addressing the great political enemies of the Big Corporations in this particular moment – the hardworking, Populist Party-supporting farmers of Kansas. (This is for rhetorical effect; I doubt too many populists were reading this attorney-specialty journal). And in this section, the editors suggest that should these farmers try to use the state power they control, they’ll face a potent force – in law, if not actually in the military.

“If Kansas attempts, through its legislation, to interfere with the sovereign prerogatives of Delaware, Delaware will be there with its oyster-boat and clam-boat navy, and with its unterrified militia; and what then will Kansas do about it?” (p.423)

And then finally, they note the alchemical aspects of Delaware’s new law.

“Let us not forget, oh, toiling brothers of the Kansas deserts, one other feature of this congenial law: 6. “The liability of the stockholder is absolutely limited when the stock has once been issued for cash, property or services.” Brother, do you need to photograph this sentence by means of an X-ray? Can you not see through it? Is it not pellucid ? It says, ” issued for cash.” It does not say paid for in cash. Is it not ” issued for cash” when it is issued for the promise of cash? and is it not issued for property or services when it is issued for the promise of such commodities? And if the gold bugs, bond- holders and other octopi, should render it hard to redeem your promise to pay for your shares – even in chips and whetstones, – why should you so pay? You have launched your corporation; the sovereign laws of Delaware allow you to commence business before any “sum whatever was paid in; ” and who or what is going to stop you from continuing your business? Do you not see that here is a scheme to turn the world into a sudden millennium? And if you object that a millennium must consist of a thousand years and cannot be created in a day, the answer is that all things are possible with the sovereign State of Delaware. What were the dreams of the ancient alchemists to this? They at most could, by processes somewhat tedious and expensive, convert gross metal into gold. But, without any gross metal of any kind to work upon, not even silver at the ratio of 16 to 1, the sovereign State of Delaware stretches forth her wand over the prairies of Kansas and calls upon money to come, and it comes.” (p.424)

What the irritated attorneys have described here is the central magic of finance, generally, and corporate finance, in particular. With some law and a bit of market faith – and a willingness to grift – you can conjure something out of nothing, and profit. Devolving sovereign power onto private parties who derive artificial persons, and then mortgage those “persons’ ” future cash flows for current income to actually do something (well, sometimes) – That’s Capitalism, Baby! If it feels like fraud, well, you probably don’t sit on the right corporate boards.

This is all to say that criticism of those would weave this kind of spell – and of Delaware legislators’ meddling in its magics, specifically – is nothing new in 2024. The First State’s legislators been catching heat for playing sorcerer’s apprentice, and carrying water for outside financial interests, for a very long time. Maybe they should get used to it? (Or, I dunno, change their ways?)

![Louis Dalrymple, “Uncle Sam’s Dismal Swamp,” Puck, November 15, 1893, https://www.loc.gov/pictures/resource/ppmsca.29155. Print shows Uncle Sam sitting on a log in a swamp labeled "Spoils System" from which snakes labeled "Quayism", "Bardsleyism", and "Tannerism", and noxious fumes rise in the form of shades labeled "Raumism - Pension Swindler, Crokerism, McLaughlinism, Tweedism, Prendergast - Political Assassin, [and] Guiteau - Political Assassin". Also shown among the tree roots is Charles A. Dana.](https://daelnorwood.com/wp-content/uploads/2025/02/dismalswampcrop.png?w=839)