Or, The Road to Hell is Paved With Private Offerings

Bipartisan Comity

I have a brief opinion piece in the Bay to Bay News today, that puts a new, bad bill in historical context – and explains why I think it will harm a lot of people.

Here’s a teaser:

It’s 2025: Do you feel like you aren’t getting scammed enough? Are you tired of not being cheated, ripped off and defrauded? Probably not. We’re drowning in spam calls, phishing emails and junk mail, all pitching shady deals. It seems like we’re under constant siege by an army of con artists — and they’re winning.

Most people would prefer that government stop these financial predators — not lead more wolves to the door.

Unfortunately, Congress has taken the side of the wolves. Led by Rep. Sarah McBride, D-Del., the House of Representatives just unanimously passed the Equal Opportunity for All Investors Act of 2025. The bill smashes down guardrails that, for almost a century, kept Wall Street sharpers from picking the pockets of regular people. Together with the Trump administration’s rush to eradicate limits on private equity’s access to your retirement savings, this legislation sets the stage for a new financial crisis.

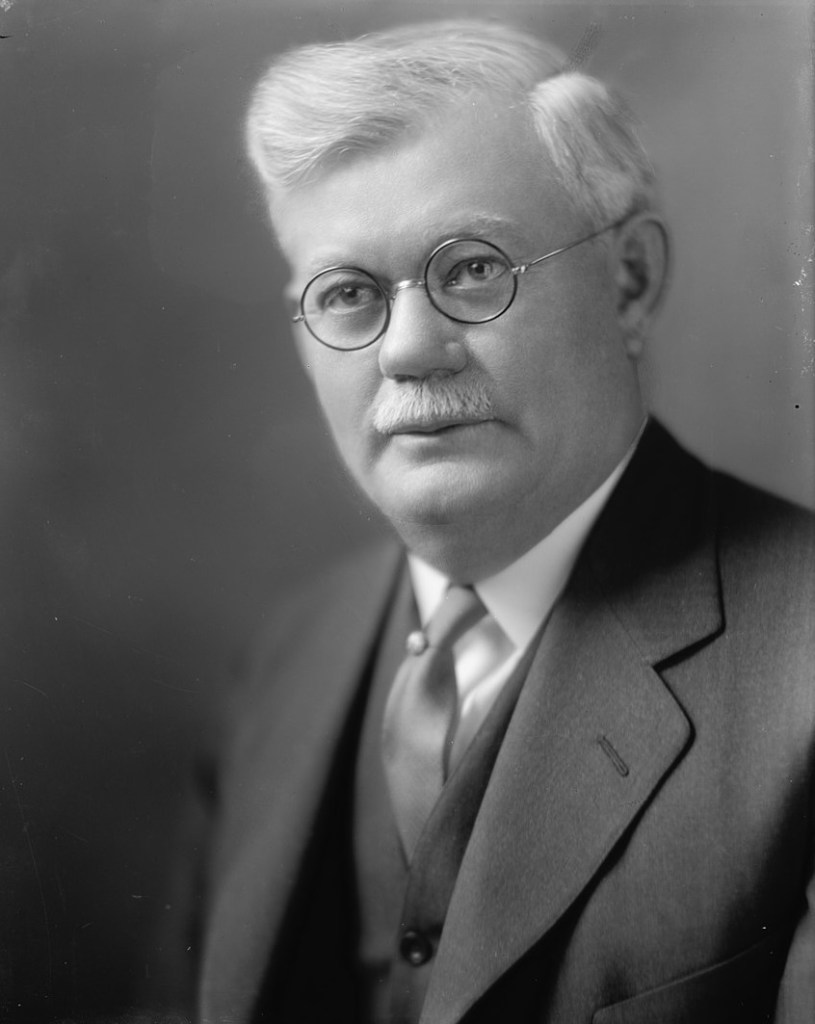

Or, a New Deal Democrat describes a Delaware Senator as … unbought?

Sen. John G. Townsend, Jr., of Delaware. Apparently not fully owned by corporate interests!

In the course of researching the political history of the Securities Act of 1933, I encountered a rather surprising description of a Delaware politician. In 1959, “Dean” James M. Landis, one of the aides primarily responsible for drafting the bill and shepherding it through Congress, published a close account of his experience getting this critical New Deal legislation off the drawing board and into the law books.

His article is a brief but quite detailed play-by-play of the political process – an Aaron Sorkin narrative, but with substance – and includes a number of deft character sketches of the various politicos and operators he dealt with as he hustled the most important federal financial regulation ever written over the finish line.

At the moment of high drama of his narrative (the House-Senate bill reconciliation conference meetings) he characterizes Senator John G. Townsend, Jr. (R-DE) this way:

“The tenseness of the first day’s session became relieved as [Rep. Sam] Rayburn made it plain that any suggestion of any Senator would receive the most careful consideration. A goodly number of suggestions came from Senator Townsend of Delaware, a Republican, who was in close touch with the financial world but who under no circumstances would take their suggestions as commands or as ideas to hold on to in the face of a compelling argument to the contrary.” [emphasis mine]

~James M. Landis, “Legislative History of the Securities Act of 1933,” George Washington Law Review 28, no. 1 (1959): 45-46

FDR’s man on the ground, a Felix Frankfurter student and Louis Brandeis protégé, a future chair of the SEC, Landis was impressed with how uncorrupted a Delaware Senator was by corporate financiers. As far as I know, that makes Townsend the first – and perhaps only – senator thusly described (certainly that differentiates him from other Delaware (state) senators who share his name…)

Or, Delaware Stands Ready To Perpetrate Any Sort of Corporate Enormity (Again)

Stock certificate, 30 shares @ $50 par, Kennebec Ice and Coal Company, January 26, 1884, Artisans’ Savings Bank of Wilmington, Delaware records, 1861-1960 (1099), Box 164, Item 31, Hagley Library & Museum (Wilmington, DE).

Mark Twain never said that “history never repeats itself, but it rhymes.”(1) But if he had taken time out to consider the past, present, and future of corporate corruption, with particular attention to the the diminution of shareholder rights, I put it to you, dear reader – he might’ve done.*

The author of the Gilded Age came to mind recently when I ran across more evidence that our simulation is caught in a loop, repeating the obvious mistakes of the past, again. William Z. Ripley (believe it or not) was who caught my attention.

In the mid-1920s, Ripley, an Ivy League social scientist and popular Progressive railroad reformer, took aim at corporate governance; or rather, the startling lack thereof. In a series of Atlantic articles and then in a 1927 book, Ripley catalogued the recent legal and financial innovations that had put “Main Street” at the mercy of “Wall Street” in new and destructive ways.(2) Though he claimed to not be any kind of muckraker (or, horrors, a socialist), Ripley still wanted to get down to the “root of things” – to diagnose how “property” and been “allowed to degenerate into an instrument of oppression” in America.(3)

Delaware, in part, was to blame. (But you knew that already.)

For Ripley, private property turned into a tool of tyranny when corporations severed ownership from control. Ripley argued that this wicked wound had first been cut by the proliferation of corporations across all lines of business – a tendency, he noted, that was peculiarly well advanced in the US, but not in Europe. That laceration was deepened by the widespread practice of watering-down corporate shareholder rights. He was particularly disturbed by two phenomena: the advent of “no-par” stock issuances, and the rise of non-voting tiers of stock.

Of the two, no-par stock bothered him more. Prior to its invention, corporations assigned each unit of stock a face-value, and printed that value (say $50) on the certificate; that amount was “par.” The buyer and holder would then know they had contributed $50 to the capital of the Kennebec Ice and Coal Company, Inc. – say – and that that amount was their claim on a particular percentage of the firm’s equity; secondary traders would also have a clear sense of how the current price of the stock compared to its initial value. If a corporation later decided to accumulate more capital by selling additional equity, common law practice before the late nineteenth century made it unlawful to offer new shares at less than the original par value – and existing shareholders had a preferred right to buy in to the new issuance, and thus keep the size of their stake equal with other shareholders.

The advent of no-par stock changed all that. In practice, no-par stock issuances meant “much below par” and sometimes “zero cost.” And for Ripley, they destroyed the moral relationship between investors and the corporation. He decried them as an “egregious malversation of the rights of shareholders and of the public generally” because they allowed companies to dilute stock, effectively robbing earlier investors of value and future buyers of much-needed information. They could also inflate the control of well-positioned insiders, like members of the board of directors, who could load up on new no-par shares to acquire more dominant voting rights.(4)

For similar reasons, Ripley opposed the proliferation of corporations issuing non-voting stock. Rooted in the deep Anglo-American legal tradition, he considered corporations to be voluntary commonwealths, premised, like all republican polities, on equality among members to function (municipalities are also a form of corporation, one might here recall…). Tiered stock structures separated equity into classes with different voting rights – building in inequality. A corporation might issue 100,000 shares, divided between 1,000 Class A shares, with rights to vote for the board of directors, and the remaining 99,000 as non-voting Class B shares – securities with no controlling powers, just vague claims to a portion (“aliquot”) of the corporation’s wealth.

Ripley thought both methods were perversions of the “essence of corporate democracy” – the premise that “all members of the company shall stand upon an even footing with one another.”(5) This posed a problem for corporate investors, internally – an inside group had means to gain control without matching their stake, and therefore the means to steal from other stockholders, by arranging sweetheart contracts for themselves, or simply by voting special dividends. It also posed a dilemma for society, at large, because in combination with holding companies and trusts, it accelerated the dispersal of responsibility for corporate actions beyond any readily identifiable individuals – common stock holders didn’t have any say on corporate decisions! –while, paradoxically, concentrating control of corporate wealth into an ever-smaller number of hands (again via holding companies). In a moment where corporations had become not just one form of economic entity among many, but the default choice for *any* and *every* form of business, Ripley saw an invitation for un-remediable theft and fraud – and documented dozens and dozens of actual instances of it.

And wouldn’t you know it, Delaware shows up as one of the authors of this disaster! Ripley traces the spread of these terrible innovations to competition between states for “chartermongering.” The race-to-the-bottom between sovereign states for charter revenue opened the door for ever-looser laws, making insider dealing between directors and controlling stockholders not only legal, but a core business strategy for modern corporations. “The little state of Delaware has always been forward in this chartermongering business,” he noted – and led in this laxity, too. (Though unlike many later Delaware lawyers and state officials, Ripley in 1927 doesn’t credit Delaware with dominating the chartermongering business; the First State is one of several mean jurisdictions, like Maine, Arizona, and New Jersey, making life worse for all Americans).(6)

Ripley is worth quoting at length about how this corrupt legislative process proceeds, partly because he really decides to go for the gusto in his language:

“But it is the evidence of an unholy alliance between private profit and the exercise of this supposedly sovereign function which is at times the most debasing in its influence. The system tends to create a horde of shysters, ready to perpetrate any sort of corporate enormity, provided only that the fees are sufficiently ample. And attorneys, on their part, as one of them writes me, ‘pick their states of incorporation as you or I would pick out a department store at which to trade.’

Another shameful angle to this business is that it tends to envelop our state legislative chambers in a noisome atmosphere of political honeyfugling, if not of downright corruption. A minor modification of a state statute may be worth large sums of money, because of its effect either upon plans in contemplation, or else as affording possible relief from the untoward results of acts already committed. And just because these amendments are seemingly so insignificant, they may be slipped through without arousing comment and perhaps almost entirely without notice. The temptation to spend money in what amounts to bribery, in order to attain such results, may upon occasion be very great. Nor need the immediate accountability for such corruption necessarily rest upon the corporations themselves. The system gives rise to a considerable body of irresponsible intermediaries — henchmen, lobbyists if you please — specialists in such branches of the law, hangers on about the state capital. The great corporation merely whispers its need. Subservient agents hasten to bring about the desired result, and perhaps no questions are asked. …”(7)

Now, if “political honeyfugling, if not downright corruption” doesn’t describe the ugly process of passing SB 21 (and its recent predecessor “reforms”), I don’t know what does.

But beyond the remarkable resemblance between Ripley’s description of how legislative corruption works at the state level – the “henchmen” and other “subservient agents” who rush a bill through are extremely familiar figures in Delaware – the substance of Ripley’s complaints about the evils of insider string-pulling toll quite recognizable tones. He’s lamenting the structural abuse of what today’s corporate legal specialists call “private ordering.” And easing the rules on private ordering for controllers is what current Delaware legislators, and their affiliated henchmen, have been gunning for, over these last few years.

There’s another thread that links Ripley’s century-old critique to today’s miseries. Ripley was an acknowledged influence on Adolf Berle and Gardiner Means, his contemporaries and the major (if constantly misread) theorists of structural problems in corporate governance. Like Berle and Means, Ripley’s concern was about the problem of control in corporations – not the divide between professional managers and stockholders owners, per se, as is usually claimed, but the one between any stakeholders in the control of the business itself.(8) Ripley, like his colleagues Berle and Means, cared about any mechanism that produced a power imbalance between members of a corporation – and in the 1920s, as now, that threat came most clearly from controlling minority shareholders, not the managers they hired.

Berle and Means are now the more famous writers – but a century ago, Ripley was a much louder and more well-known voice.(9) Over the next decade his profile only grew in prominence, because, among other things, he predicted the Great Depression (which … other famous economists quite infamously did not). Ripley’s concerns with corporate opacity, controlling shareholders, and insider dealing contributed directly to the New Deal reforms that came less than a decade later, after the crash (and specifically the federal Securities Exchange Act of 1934). It’s not a stretch to say that the Ripley’s specific complaints shaped the specifics of financial regulation in the United States, at least until recently.

Which leads me back to my sense of chronological vertigo. In the last few years, the Delaware General Assembly has taken a hacksaw to shareholder rights, reversing judicial rulings that had curtailed the amount of insider dealing (“private ordering”) that corporate boards could do. Alongside this strangling of the main venue for private redress of corporate wrongs, federal regulatory agencies, most notably the SEC and CFPB (but increasingly the Federal Reserve, too), have been captured or closed outright – eliminating the public arm of corporate regulation. The nation’s feeble protections against the same corporate fraud and thefts Ripley decried are now dead letters in their state and federal forms – and controlling shareholders are free, once again, from any restraints that bound them from freely picking the pockets of fellow shareholders, and citizens.

Thus, the unbound and unaccountable corporate immorality that Ripley decried in his own time – the oppressive property of corporate property – is back again, a boot pressing on all of our necks. Which makes it all a bit rich – or perhaps a bit ironic? – that the group of Delaware legal professionals, academics, jurists, and defense attorneys, who are – putatively – among most familiar with Berle and Means (and, thus Ripley, one step removed) should have been the intellectual architects of this repeat disaster.(10)

One can only hope that long dead Progressives like Ripley retain the capacity to haunt their traitorous professional descendants, even as the rest of us are horrified by the specter of what Delaware has, once again, wrought.

——

A brief note: This is not a William Zebina Ripley fan account. He was one of the most influential writers on modern scientific racism. He came to national prominence first, not for his scholarship on colonial finance, railroad management, or corporate governance, but for his 1899 book, The Races of Europe. Originally developed as a lecture series at Columbia University and at the Lowell Institute, it’s a fantastically stupid piece of work, exemplary of the time, filled with tedious ethnic and racial stereotypes “proven” by tendentious skull measurements. It was, of course, a huge hit with eugenicists, white supremacists, and other evil, awful people, both in the US and abroad – including Madison “Hitler’s My No. 1 Fan” Grant. Ripley’s intellectual legacy has a body count in the hundreds of millions – and one that grows by the day, as his theories persist through the AI-“trained” ideas drug-addled billionaires and quack failsons have used to justify horrific revisions in US federal policy. He’s also from Medford, MA (derogatory).

1. As far as I know, Twain never used the phrase, exactly – though in his 1873 co-written novel, The Gilded Age, a character quotes a newspaper offering a similar sentiment:

“History never repeats itself, but the Kaleidoscopic combinations of the pictured present often seem to be constructed out of the broken fragments of antique legends.”

Quote Investigator finds the closest instance of this phrasing in a poem by John Robert Colombo – in the text, the phrase is attributed to Twain. John Robert Colombo, “A Said Poem,”Neo Poems, p. 46.

8. As historians Ken Lipartito and Yumiko Morrii note, “[t]he conflict that Berle and Means emphasized was not between managers and owners, but between owners and owners.”Kenneth Lipartito and Yumiko Morii, “Rethinking the Separation of Ownership from Management in American History,”University of Seattle Law Review 33, no. 4 (2010):1048; on Berle and Means’ relationship to Ripley, see p. 1045-46 (though note that Lipartito and Morrii misdate the publication of Ripley’s “exposé” in the text to 1928; it was 1927).

9. He got a lot of positive press, and was recognized as sufficiently prominent to scare the NYSE in to pretending to act to prevent no-par stock issuances. Ralph W. Barnes, “A Professor Who Jarred Wall Street,”Brooklyn Eagle (New York), April 18, 1926; S. T. Williamson, “William Z. Ripley –and Some Others,”The New York Times, December 29, 1929. (He also made the news wires when he was injured in a car accident in Manhattan, riding with a woman who wasn’t his wife. See, for ex: “Prof. Ripley in N.Y. Taxi Crash,”Transcript-Telegram (Holyoke, Massachusetts), January 20, 1927; “Noted Economist Hurt in Crash,”The Herald Statesman (Yonkers, NY), January 20, 1927.

Or, It’s Time to Imagine a Future Beyond the Franchise

Lyman Beecher – a guy who saw some downfalls and declensions in his time

The Delaware franchise has been under serious attack for some time. Leading the charge are the richest men in the world, billionaire tech financiers, who see in Delaware law an outrageous affront to their power.

The conflict is something of a tragic irony for First State jurists. Emerging from the coddled confines of Palo Alto office parks, Manhattan penthouses, and group chats, these monied men understand themselves to be heroic innovators rather than well-placed directors of capital flows, men of history who are by dint of genetic excellence and genius effort elevated beyond the common clay. They therefore bristle at what a prior generation regarded as the final victory of Friedmanite ideology, viz., Delaware’s judge-made law that requires all business decisions to be made in favor of shareholder gain, and nothing else.

For anyone outside the cult of Gordon Gekko, it’s clear that the federalist jujitsu that’s made Delaware’s perverse insistence on shareholder primacy and short-term profit go global has been a disaster – for human health and flourishing, generally, and democracy in the United States, specifically. But for our modern robber barons, the application of judicial restraints – even for the purpose of maximizing shareholder gains! – has been as enraging and painful as a public flogging. In retaliation for this keenly felt but entirely imaginary insult, they and their servants in the corporate law world have fanned the flames for “DExit.” The goal, transparently and repeatedly announced, is to punish Delaware, and especially its judges, by denying the state the corporate franchise fees and escheats upon which it has grown dependent. They want to starve the horse they rode in on.

Delaware’s governors and legislators have responded to these attacks with abjectcapitulation. But since the root of the conflict lies in rich narcissists’ hurt feelings, appeasement has not worked. Instead, attacks have continued. In the past week, leaders of the world’s largest VC firm, known for hiring homicidal vigilantes, proudly declared they were “Leaving Delaware” and invited others to do likewise, in order to escape Delaware’s onerous bias “against technology startup founders and their boards.”

Leaving aside the bizarre dissembling involved with officers of an LLC claiming they will change the “state of its incorporation,” the conclusion that must be drawn from this latest tantrum is that the fuel for “DExit” is far from finished. True, the corporate stampede that SV billionaires have attempted to kickstart has not yet caught on. But given the power this cohort of corporate aristocrats wields – oceans of capital, vast media megaphones, and a keystone place in the revanchist coalition governing the United States – a future in which Delaware’s corporate franchise is crippled, or killed outright, seems a distinct possibility.

So what happens when the standing order of a state comes crashing down?

~

In 1818, the State of Connecticut adopted a new constitution, and disestablished the Congregational church. After almost two centuries of legally mandated taxpayer support, the state’s church was overthrown – out-muscled by a coalition of Democratic-Republican partisans and rival Protestant denominations, who took the opportunity of the Federalist Party’s decline to crack the central pillar of Connecticut’s “Standing Order,” and wedge in a measure of religious freedom in the bargain.

The war for disestablishment was fiercely fought for years. Lyman Beecher, a popular and ambitious Congregationalist minister, was among the leading anti-disestablishmentarians. In his early forties when the institutions that defined his life and successful career started to totter, he worked frantically to shore them up, organizing political supporters and leading evangelical revivals “with all [his] might” to salvage what he regarded as humanity’s last best hope for salvation.

Beecher worked until his “health and spirits began to fail,” but he and his co-religionists still lost – and fell into grief when they were beaten. Harriet Beecher Stowe, his daughter, remembered that when news of the key election loss arrived at their home, “a perfect wail arose.” Beecher himself recalled the period was “as dark a day as I ever saw” (quite a thing for a guy living in an era of high infant mortality to say).

However, in time, he changed his mind.

“I suffered what no tongue can tell for the best thing that ever happened to the State of Connecticut.” [emphasis in original] [1]

In describing disestablishment this way, Beecher didn’t mean that the state itself benefited, as a government. He meant that society as a whole did. Being thrown “wholly on their own resources and on God” increased ministers’ influence, he argued, by forcing their evangelizing to go to ground – to save souls through “voluntary efforts, societies, missions and revivals” rather than through coercive force or the trappings of wealth and power. Disestablishment, for Beecher, furthered God’s cause by making it more authentic, and thus more popular.

Beecher came to this perspective after a long life of successful (and controversial) evangelical work. He was also riding a tsunami of transformative evangelical fervor in the Second Great Awakening, a wave of dramatic cultural change with origins, energy, and effects that drew on waters far deeper and wider than any in the Nutmeg state.

Still, I think Beecher’s late-life observation is worth keeping in mind, particularly when considering changes in a state’s political economy that might seem apocalyptic. He saw the downfall of the Connecticut’s Standing Order, an establishment much sturdier and long-lived than any kind of Delaware Way, and lived to call it a blessing.

And yet, change comes. As Ursula Le Guin explained, “[w]e live in capitalism. Its power seems inescapable; so did the divine right of kings.” In that moment, Le Guin was contemplating art amid Amazon’s growing monopoly, but she did so with a historical sense that stretched beyond Bezos’s horizons, and an anthropologist’s awareness of how all human societies, like human beings, are mortal.

Delaware’s corporate franchise is itself transitory. As Vice Chancellor J. Travis Laster has recently observed, “[f]or the first 120 years of Delaware’s existence, corporations were no more significant to Delaware than to any other state.”[3] Delaware, as a self-governing polity, has existed for a handful of years longer under its current corporate configuration than it has without it – but the years where franchise revenues were critical to state finances are many fewer than that. Delaware’s current political economy has a history – and it’s not a long one, nor inevitable.

That’s important to keep in mind today, when the power of the franchise seems both inescapable and irresistible. It’s a force that routinelyturnspoliticianswho ran (and wrote!) as progressives into staid corporatedefenders, and constantly skews governing priorities toward ends that do substantial social harm, in Delawareand beyond. By setting up shop as the preeminent caterer for corporate whims, Delaware has caught the corporate “wolf by the ear,” and can neither function as a state without depending on its revenue, nor function as a representative democracy within that dependence.

But if Delaware is to get to that outcome, some study and planning for that future is needed, now. This year, the legislature has invested in research to maintain the status quo, but a serious effort for a truly forward-thinking and realistic agenda will require something different. [4]

Some questions Delaware must answer:

What sources do similarly small states rely on for revenue? Rhode Island persists, without a franchise; could Delaware?

How much could a sales tax bring in – and what rate would maximize revenue while minimizing the burden on the least able to afford it? What kind of transition procedure would be least disruptive?

Delaware Democrats recently quashed an effort to update personal income tax brackets to make them more equitable. Could a successful effort capture sufficient revenue from high-income earners to make up for a portion of franchise losses? (Ironically, in this case the actors most responsible for the “DExit” flight – corporate defense lawyers – may be the most directly able to bear new taxes to make up its loss).

The Delaware State Bar claims that corporate law services bring in billions, but the industry’s economic impact has not been rigorously studied by independent researchers.[5] What is the industry’s true value, and what effect will the decline and loss of the franchise have on employment, and public revenues? If billionaires and tech corporations abandon the state, but LLCs and other business entities continue to be formed here, what effect will that have on court usage and lawyers’ employment?

Finally, it would be well to expand our historical understanding of the franchise. Shockingly little is known about the actual operations of the franchise in the past, or its development, as a functioning support for government. When did Delaware become dependent on the corporate franchise for revenue – and how did that process unfold? Recent research suggests the oft-repeated story, that Delaware’s dominance of the corporate charter market started with New Jersey’s fall in 1911, has a severe evidence problem.[6] So when did things start to change, who drove it, and with what consequences? A firmer grasp of the facts of what happened would, I suspect, change our ideas about what is possible.

The life or death of the corporate franchise is not a matter within Delawareans’ control. That, in itself, is a reason to want to diversify the state’s revenue sources. But even if First State politicos are unwilling to quit the gravy train cold turkey, their dealers seem ready to cut off the supply, nonconsensually.

In either case, its time for Delawareans to start thinking hard about what a future without the franchise might mean – the problems it would bring, but also the opportunities. Because stasis isn’t just unlikely; it’s impossible.

—–

[1] Lyman Beecher, Autobiography of Lyman Beecher, ed. Barbara M. Cross (Cambridge: Belknap Press of Harvard University Press, 1961), 1: 252-253

[3] J. Travis Laster, “An Eras Tour Of Delaware Corporate Law,” Journal of Corporation Law 50, no. 4 (July 2, 2025): 1189–1263, https://jcl.law.uiowa.edu/articles/2025/07/eras-tour-delaware-corporate-law. Laster, as a jurist, is rather looser with chronology than any persnickety historian would be: Delaware’s period of “normal” corporate engagement lasted 123 years, while its era of eager corporate solicitation has lasted 126 (so far). That said, the article is a valuable exercise in periodizing legal history, and offers readers many claims worthy of further investigation and research.

[4] In it’s most recent session, the Delaware General Assembly reserved $200k for research into the “corporate franchise,” and sponsored a resolution directing the “AI Commission” and the Secretary of State to study AI’s uses for “corporate governance.” It seems unlikely that either effort will result in measures that improve democratic outcomes. See: HB 230, “An Act Making Appropriation for Certain Grants-in-Aid,” July 1, 2025, Section 19; and HJR 7 w HA 1, “Directing the Artificial Intelligence Commission,” June 30, 2025.

[6] Andrew Verstein, “The Corporate Census,” SSRN Scholarly Paper (Rochester, NY: Social Science Research Network, February 25, 2025), https://papers.ssrn.com/abstract=5154952

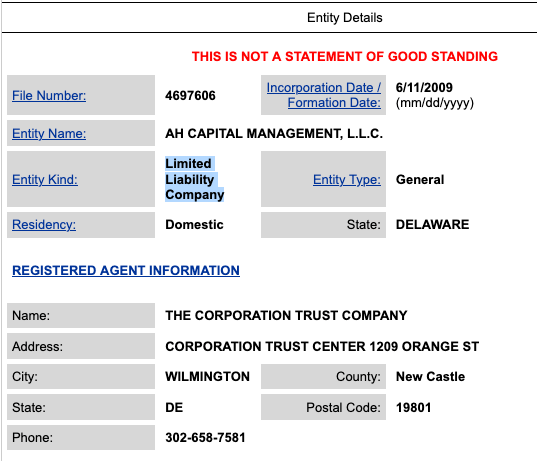

Greetings, I hope this finds you well. I wanted to bring a recent piece of news to your attention, as it bears on the General Assembly’s treatment of corporate law.

Here’s the thing, though: Andreessen Horowitz (AH Capital Management) is not a Delaware corporation. It’s a Delaware LLC.

As a limited liability company, it can’t “move” its incorporation anywhere; it doesn’t exist. More to the point, none of Andreessen Horowitz’s complaints about Delaware apply to their firm, or to any of the subsidiaries they have registered here as LLCs or Limited Partnerships (LPs), as a quick search of the DE Division of Corporation Business Entity Filing database will attest. This distinction is not a mere matter of synonyms, but one with material consequences for how a business operates. As legal scholars have observed, “An LLC By Any Other Name Is Still Not A Corporation.”

It seems unlikely that the leaders of the world’s wealthiest venture capital firm cannot distinguish between two basic types of business entity structure. It seems equally unlikely, then, that Andreessen Horowitz’s decision to leave Delaware is motivated by their stated reasons. Their critique, in other words, appears to be made in bad faith.

As you and your colleagues contemplate further revisions to Delaware’s corporate law, I urge you to keep this evidence of deceptive arguments from Delaware’s critics in mind – whether they come from business owners, directly, or the locally influentiallegal advocates they employ.

Sincerely, your constituent, DN

NB: most of the outlets reporting on this move – NYT, Bloomberg, Inc – reproduce Andreessen Horowitz’s statement without comment, and thus its errors.